Wheaton Precious Metals(NYSE: WPM) is one of the larger streaming and royalty companies, competing with peers like Franco-Nevada(NYSE: FNV) and Royal Gold(NASDAQ: RGLD). While it effectively operates in the gold and silver space, it isn't a miner. That changes the equation for investors in some important ways. If you are looking to add precious metals to your portfolio, Wheaton could be a good fit. Here's what you need to know.

An alternative to mining stocks

Building a gold or silver mine is very expensive. It is also very risky. The process basically involves finding a location that might contain precious metals, getting approval to build a mine, building the mine, operating that mine until the mine is no longer profitable, and then, usually, returning the mine site back to its pre-mine state. Things can go wrong during any one of the steps on that list.

Image source: Getty Images.

For example, a mine site could turn out to be a dud if the quality of the ore isn't up to expectations. A great mine site could face legal and regulatory pushback, drastically increasing costs, causing delays, or, perhaps, even leaving the site undeveloped. There's major execution risk in any construction process, particularly when it involves digging massive holes in the earth. And it is pretty common for mines to get hit with employee work stoppages.

That's where streaming and royalty companies like Wheaton come in. Because Wheaton doesn't own or operate mines, it doesn't have to deal directly with any of these issues. Instead, Wheaton and its peers provide cash to miners in exchange for the right to buy precious metals at reduced prices. Usually the cash comes first to help miners build or expand mines. Once the mines and expansions are up and running, and thus producing precious metals, Wheaton gets the opportunity to buy silver and gold at advantaged prices.

Wheaton is really a financial partner that gets paid in precious metals, when you step back and look at the big picture. This is good for the miners because they don't have to sell stock or take on debt to build out their operations. It is good for Wheaton because it avoids a lot of mining risks and gets to buy precious metals cheaply. And it owns a collection of streaming and royalty agreements that provide more diversification than you would normally get from an investment in a single miner. It earns money by offering the cut-price metals it buys for resale at market prices.

Wheaton's big benefits

To be fair, Royal Gold and Franco-Nevada follow the same basic business model. So why would you want to own Wheaton over either of these two notable peers? There are two worthwhile reasons.

For starters, Wheaton generates around 97% of its revenues from gold, silver, and other precious metals (like platinum). A tiny 3% comes from cobalt, which is a key battery metal, a fact that might attract some to the stock even though precious metals are the real driving force. That 97% compares to 83% for Royal Gold and 70% for Franco-Nevada.

There are reasons why these other companies have lower figures. For example, Franco-Nevada has added energy (oil and natural gas) to its mix for diversification purposes. But if you are looking specifically for exposure to precious metals, then Wheaton is going to give you the biggest bang for your buck.

Speaking of bang for buck, Royal Gold and Franco-Nevada both have very predictable dividends. They focus on providing investors with regular annual increases, which, given the inherent volatility of commodity prices, means passing less than they probably could on to shareholders during precious metals upturns. That might be exactly the type of consistency that some investors want.

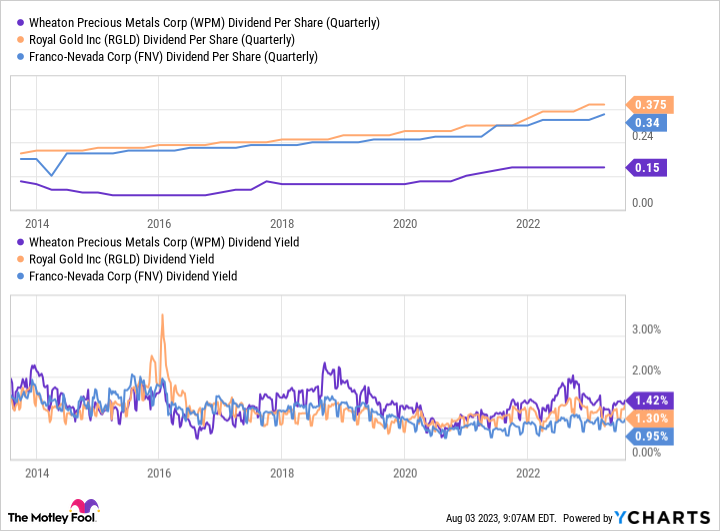

WPM Dividend Per Share (Quarterly) data by YCharts

Wheaton has a variable dividend policy: "The quarterly dividend per common share will be equal to 30% of the average cash generated by operating activities in the previous four quarters divided by the Company's outstanding common shares at the time the dividend is approved, all rounded to the nearest cent." Essentially, when the company is doing well, you are likely to benefit from higher dividend payments. But, in exchange for that upside potential, you are expected to share in the pain when falling commodity prices lead to weaker results.

That's a reasonable trade-off, considering that Wheaton's 1.4% dividend yield is slightly higher than the 1.3% offered by Royal Gold and well above the 1% you can collect from Franco-Nevada currently. As the chart above shows, a higher-than-peer yield isn't at all unusual for Wheaton, hinting that the investors have priced in the risk of dividend cuts.

One big thing to keep in mind

There are many reasons to like Wheaton Precious Metals as a way to add diversification to your portfolio, including the streaming model, the company's heavy focus on precious metals, and its variable dividend. But there's one thing that even Wheaton can't avoid, and that is the normal ups and downs of gold and silver prices. The company's financial results and stock performance are likely to track along with commodity prices over time, and there's really no way to avoid that.

But if you are looking for a gold and silver investment, without the business risks involved with owning a miner, Wheaton could be a great long-term holding.

10 stocks we like better than Wheaton Precious Metals

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Wheaton Precious Metals wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 1, 2023

Reuben Gregg Brewer has positions in Franco-Nevada. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.