Investors often have different goals. Some investors may be looking to simply get the highest returns possible, while others may be looking for a solid stream of income that comes from dividends.

For the latter group, determining whether a stock's dividend is safe is of the utmost importance. Dividends can be cut due to underlying issues, which isn't something income-oriented investors like to see and usually causes a stock to tumble. As such, it is often best to avoid these situations.

Let's take a look at two stocks with ultrahigh yields with super-safe dividends.

1. Altria Group

Tobacco giant Altria Group(NYSE: MO) has long been a favorite of income-oriented investors. The stock currently sports a juicy 9.6% yield, and the company has consistently increased its dividend payment for the past 15 years.

When looking into the safety of a dividend, the first place to look is the company's cash-flow statement. The reason is that dividends are paid from a company's free cash flow. If the dividend exceeds a company's cash flow for an extended period of time, there is a high likelihood it could be cut in the future.

For 2023, Altria paid $6.8 billion in dividends to its shareholders. Meanwhile, it generated free cash flow, which is operating cash flow minus capital expenditures, of $9.1 billion. As such, the company paid about 75% of its cash flow toward its dividend, which demonstrates a high degree of coverage and gives the company room not only to maintain its current payout but also to increase it in the future. Any number over 100% could indicate that a dividend cut could happen in the future.

The other important aspect to look at when it comes to the safety of a company's dividend is its leverage, which is its net debt divided by its earnings before interest, taxes, depreciation, and amortization (EBITDA). The reason for this is because if leverage becomes too high, companies could be forced to cut their dividends in order to pay down their debt loads. Altria ended 2023 with leverage of 2.2 times, which is solid given its free cash flow.

Last month, Altria also sold 35 million shares of Anheuser-Busch InBev it owned for $61.50 per American depositary share (ADS). It then took the proceeds to help buy back $2.4 billion of its own shares. The reduction in shares will lessen the total cash Altria will pay in dividends, improving its payout ratio.

All in all, Altria appears to have a super-safe dividend.

2. Vector Group

Another tobacco stock with an attractive yield is Vector Group(NYSE: VGR), which sells discounted cigarettes and owns a portfolio of real estate. The stock yields about 8.1%.

Looking at the same metrics as Altria, Vector paid $126.2 million in dividends in 2023. The company produced free cash flow of $199.4 million, which meant its payout ratio was only 63%. However, the company does invest in real estate, but even taking into account its $17.4 million in real estate investments made in 2023, its payout ratio was 69%, below that of Altria.

Looking at its balance sheet, Vector ended 2023 with leverage of 2.6 times when taking into account cash and investments at its holding company. That is slightly higher than Altria but also solid.

Vector did slash its dividend in 2020 but for good reason, as its dividend payments were more than its operating cash flow.

For example, in 2019 the company paid $238.2 million in dividends but only had operating cash flow of $124.1 million. Dividend payments outstripped cash flow the proceeding two years as well. That is not something that is sustainable, and with debt starting to increase, the company decided to cut its quarterly dividend in half to 20 cents per share starting in the first quarter of 2020, where it has remained.

However, its dividend payout ratio and leverage are now both in good places. At the same time, the company has been gaining market share as it expanded its deep-discount brand Montego to all U.S. markets in 2021. That helped bring its market share from 4.1% in 2021 to 5.5% in 2023. Given Vector's smaller size, it is also currently exempt from the 1998 Master Settlement between states and tobacco companies, giving it a cost advantage over larger players.

Image source: Getty Images.

High yields at discounted prices

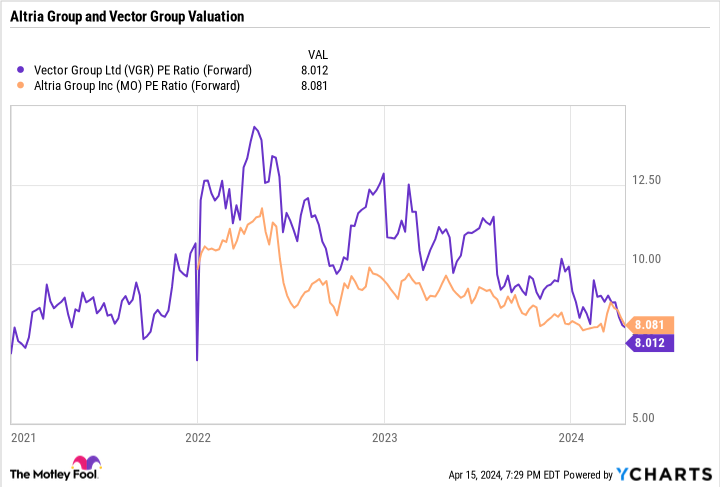

Both Altria and Vector trade around 8 times forward price-to-earnings (PE), which is inexpensive on a historical basis. While the stocks have struggled over the past year, their yields have climbed to attractive levels. At the same time, both dividends look very safe.

VGR PE Ratio (Forward) data by YCharts.

Now could be a good time for investors to jump into these two tobacco stocks given their valuations and yields. Both dividends are currently well covered, and their balance sheets are solid.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 15, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.