Things have gone from bad to worse for Spirit Airlines(NYSE: SAVE) in 2024. After its proposed merger with JetBlue Airways was blocked, the stock fell. Then, the company started to report earnings figures with growing losses as the discount airline model loses its appeal in the United States. The stock fell some more. As of this writing, shares of Spirit Airlines have fallen 84% this year and are now down 97% from all-time highs to $2.58 a share. Ouch.

Is this the bottom for Spirit Airlines? I don't think so. I predict the worst is yet to come for this embattled company teetering on the brink. Here's why things may get even worse for Spirit Airlines stock over the next few years.

Losing the JetBlue merger

In January 2024, a judge ruled against the merger of JetBlue and Spirit Airlines. The ruling was given because the courts thought a merger would reduce competition and raise prices for airline travelers, an idea that revolved around raising ticket prices on Spirit routes once they became a part of JetBlue.

Since the Spirit business was struggling before the ruling, its stock collapsed in the weeks following. In fact, this made up the majority of the stock's drop in 2024, falling from over $15 to just $5 in a few weeks. But today, Spirit Airlines stock trades at just above $2.72, having fallen even further in the summer months. Why? Because its business is deteriorating rapidly.

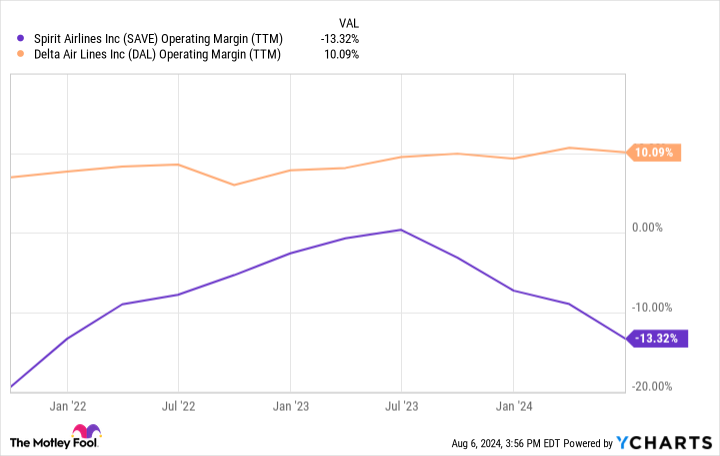

No profits despite a travel rebound

In the first six months of 2024, Spirit Airlines' revenue has fallen 8.5% to $2.55 billion. With rising costs such as aircraft rental agreements, operating income has collapsed. Over the last 12 months -- a period during which most airlines were profitable -- Spirit posted a $683 million operating loss. That is an operating margin of negative 13.3%. For reference, Delta Airlines has a positive 10% operating margin. Even though the industry is thriving, Spirit Airlines is losing money.

Airlines are now much different businesses than a few years back. With the rise of travel credit cards, customers would rather lock in airline points at a certain carrier than get a slight discount on a Spirit Airlines flight. Plus, Spirit Airlines has a rough reputation that has only gotten worse in recent years. Customers look to be finally fed up even though a Spirit flight can cost significantly less than one a mainstream airline.

Whatever the reason, Spirit Airlines is not profitable and hasn't been since the start of the COVID-19 pandemic. Its cash flow looks even worse. Free cash flow was minus $785 million over the last 12 months, its worst cash burn ever. In fact, Spirit Airlines has not generated positive cash flow since 2014.

SAVE Operating Margin (TTM) data by YCharts

A teetering balance sheet means trouble ahead

Bad cash burn means Spirit has taken on a lot of debt in order to operate. Yes, you guessed it, this has destroyed its balance sheet. At the end of last quarter, Spirit had less than $1 billion in cash compared to over $3 billion in long-term debt and close to $4 billion in operating lease liabilities.

The math just doesn't work with its current cash burn. In 12 months, Spirit Airlines will run out of cash. And even if it stems its cash burn, there is no capacity to pay its operating leases and financial debt with cash on hand.

Putting it all together, I think it is likely Spirit Airlines runs out of money soon, which would cause the stock to collapse even further. It has no merger prospects, negative margins when the industry is thriving, and a debt-laden balance sheet. Avoid buying the dip on Spirit Airlines stock unless the company can put together a miracle turnaround.

Should you invest $1,000 in Spirit Airlines right now?

Before you buy stock in Spirit Airlines, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Spirit Airlines wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $638,800!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends Delta Air Lines. The Motley Fool has a disclosure policy.