Airlines are a tough business. They always have been. It's even tougher if you promise to be a low-cost provider but can't run your business without generating a profit. That is the position Spirit Airlines(NYSE: SAVE) finds itself in. After a botched merger with JetBlue, the company is reeling as cost overruns, and the hypercompetitiveness of the airline market cause it to bleed cash flow.

Spirit Airlines is down a whopping 82% this year and 97% from all-time highs. At a stock price of $2.80, is it smart to buy the dip on Spirit Airlines stock at this bargain basement price? Let's take a look and find out.

A broken deal and worsening cash flow

Spirit Airlines was supposed to be acquired by JetBlue in early 2024. However, a judge blocked the merger over anti-competitive concerns. Spirit Airlines is now forced to operate on its own, which caused the stock to fall over 50% the week of the announcement.

Since then, shares have continued to fall. Why? Because Spirit's business keeps deteriorating. In the first quarter of 2024, Spirit reported a negative 16.4% operating margin and revenue that declined by 6.2% year over year. The company is struggling for many reasons, including the fact that its low-cost ticket model has never been profitable (free cash flow has been negative for the last 10 years). It also is facing a headwind from a new flight attendant agreement, which will see salaries rise by 40% in a few years.

Now, Spirit has updated investors yet again with preliminary results for the second quarter. The company now expects worse revenue and operating margins than previous management guidance, which has investors bearish on the stock yet again. It will no doubt negatively impact free cash flow. Over the last 12 months, Spirit Airlines has burned $781 million in free cash flow.

Is there a liquidity crisis coming?

The income statement is in bad shape, but Spirit Airlines' balance sheet may be even worse. The company has just under $1 billion in cash on the balance sheet, $157 million in short-term debt, and over $3 billion in long-term debt. The company is burning close to $800 million in cash a year, a number that is only getting worse.

Within a year or two, Spirit Airlines may face a big liquidity crisis and struggle to pay its bills. Management will undoubtedly work to avoid any sort of crisis by reworking deals or extending debt maturities. But the fact of the matter is that Spirit Airlines is in a precarious spot at the moment, and its financials are only getting worse. This should be of great concern to anyone thinking of buying the stock right now.

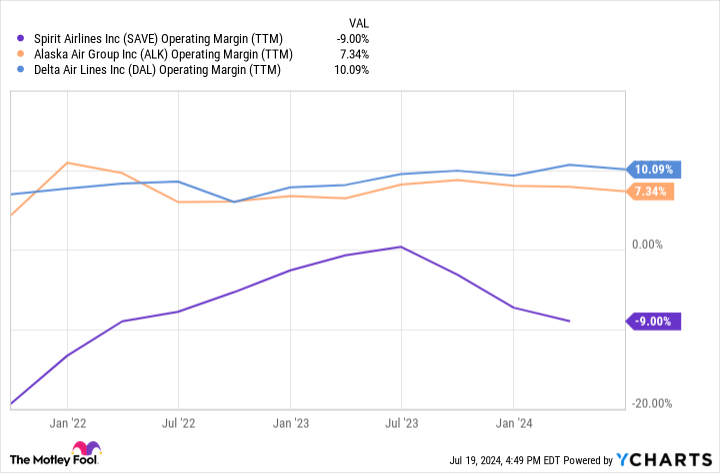

SAVE Operating Margin (TTM) data by YCharts

Avoid buying this stock

Even though the stock looks cheap because of the low share price, Spirit Airlines is no bargain. It comes saddled with debt, is running out of cash, and has a terrible operating history. The company is posting heavy free cash flow losses and has burned billions in free cash flow over the last 10 years. The low-cost airline model does not seem to be working in the United States.

If you want to buy an airline stock, a better bet is to look at industry leaders who are actually profitable, such as Delta Air or Alaska Air. Both have posted more consistent positive profit margins and trade at reasonable earnings ratios.

Better yet, you should avoid investing in airline stocks altogether. Many of these companies fail, filing for bankruptcy and selling their plane assets in an auction. The industry is hypercompetitive, with consumers remaining unloyal to any one brand. Just because a stock is down so much and trades at a low price below $3 does not make it a good buy. Avoid buying Spirit Airlines until further notice.

Should you invest $1,000 in Spirit Airlines right now?

Before you buy stock in Spirit Airlines, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Spirit Airlines wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $722,626!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 15, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool recommends Alaska Air Group and Delta Air Lines. The Motley Fool has a disclosure policy.