Just when it looks like the stock's rally is out of fuel, Spirit Airlines(NYSE: SAVE) finds a way to send its shares even higher. Today's near-20% jump is being driven by another round of news that the struggling airline may yet find a way to sidestep a potential bankruptcy.

Another step in the right direction

It's been a storied week for the company to say the least. Last Friday its credit card processor (U.S. Bank National Association) granted Spirit an additional two months to refinance its debt, providing the airline with much-needed room to improve its current fiscal situation before approaching lenders.

Then on Wednesday, whispers of an acquisition resurfaced. The Wall Street Journal's report suggested Frontier Airlines was considering making an offer for the distressed rival airline that hasn't turned a quarterly profit since the middle of 2020.

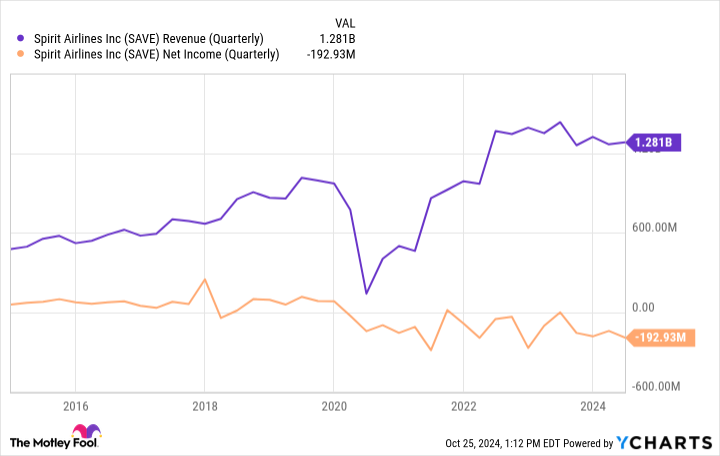

SAVE Revenue (Quarterly) data by YCharts

Heavily indebted Spirit Airlines isn't simply waiting for partners and potential suitors to solve its problems, however. It's taking action in the meantime to come up with desperately needed cash. Following Thursday's close the company disclosed it would be selling 23 of its passenger jets for a total of just under $520 million. It added that the corresponding reduction in its workforce would cull another $80 million worth of annualized operating expenses.

This news rekindled gains made by the stock earlier this week, reversing Thursday's lull.

Too far gone to salvage now

Kudos to Spirit for taking swift and sizable action. Many companies would have done less, and done it slower, simply hoping business would turn around. CEO Ted Christie recognizes it's better for a company to solve problems on its terms rather than a creditor's or bankruptcy court's terms.

Unfortunately, Spirit is too far underwater for any such effort to matter enough now.

Sure, the aforementioned sale of some of its aircraft will remove $225 million worth of debt from its balance sheet in addition to generating $520 million in proceeds. The company will also save an additional $80 million per year as a result of the sale.

Spirit Airlines is regularly losing between $100 million and $200 million per quarter though, with no end in sight. Indeed, the sale of 23 of its roughly 215 passenger jets will only make it more difficult to generate revenue, and therefore earnings. Meanwhile, the airline's balance sheet is bogged down by roughly $7 billion in long-term debt and lease obligations. Relief of $225 million isn't going to make a dent in that burden.

The best possible outcome for Spirit Airlines is still arguably bankruptcy, or an acquisition by another airline that wants its brand name and routes and doesn't mind taking on Spirit's debts and other obligations. Of course, any such offer is going to be a lowball bid.

Whatever's in the cards, there's too much risk and not enough reward to become a shareholder here.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $20,991!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,618!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $406,922!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 21, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends U.S. Bancorp. The Motley Fool has a disclosure policy.