The recent dividend cut at the Brookfield Real Assets Income Fund(NYSE: RA) led to a significant fall in the share price and called into question the sustainability of dividends in many closed-end funds. As such, I decided to look at one of them, the Guggenheim Strategic Opportunities Fund(NYSE: GOF), to help illustrate what investors should look for before investing money. Here's the lowdown and why some look like risky investments right now.

Closed-end funds with massive yields

It's not hard to see why closed-end funds are attractive to investors. Not only do many of them come with mid-teens yields right now, but they tend to invest in a myriad of assets, which helps diversify risk. Fund shares are listed on stock exchanges and have varying degrees of liquidity. In addition, closed-end funds can use leverage to attempt to generate outsized returns and dividends for investors.

Still, there's no reward without taking risks, and as investors in the Brookfield Real Assets Income Fund discovered recently, closed-end fund distributions are not set in stone. It makes sense to spend a little time looking at publicly available information before buying into one.

A quick look at a few closed-end funds shows some hefty dividends are available on these instruments. It also reveals some significant premiums-to-net asset value (NAV). The exception to the rule on premiums is the Brookfield Real Assets Income fund because the distribution was slashed recently, and the stock price is down 33% over the last year.

Closed-End Fund | Price | Net Asset Value Per Share | Premium-to-Net Asset Value | Yield |

|---|---|---|---|---|

Brookfield Real Assets Income | $12.91 | $14.7 | (12.2)% | 10.6% |

PIMCO Dynamic Income Fund | $18.03 | $16.93 | 6.5% | 14.7% |

Guggenheim Strategic Opportunities Fund | $15.72 | $12.32 | 27.6% | 13.9% |

Cornerstone Strategic Value Fund | $8.32 | $6.92 | 20.2% | 17.7% |

Data source: Yahoo Finance.

Four things to look for in closed-end funds

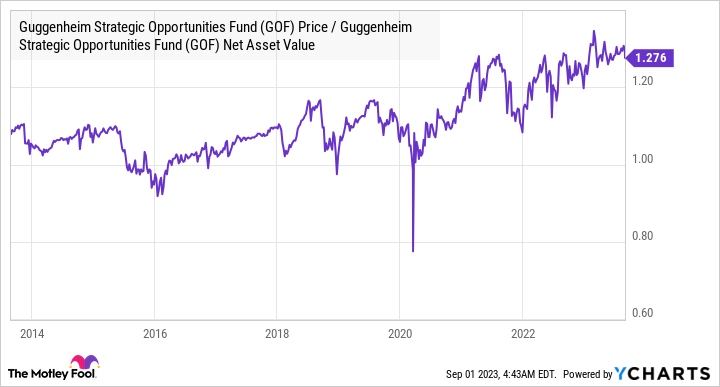

Investors must first consider the premium or discount to net asset value. Recalling that the Brookfield fund traded at a premium to NAV before the recent crash, the Guggenheim premium looks very high. Indeed, it's high historically and implies that market sentiment currently favors the fund's ability to generate returns for investors.

Fundamental Chart data by YCharts.

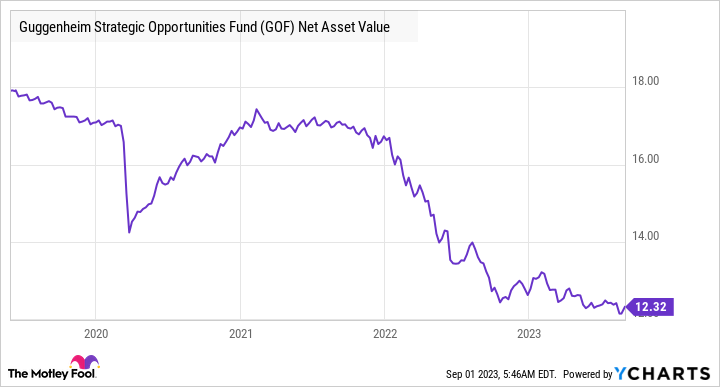

Look at net asset value

The premium seems somewhat inconsistent, though, with the deterioration in the fund's NAV this year. This point leads me to the second thing to look for. Check the direction in the NAV and the assets it's holding.

GOF Net Asset Value data by YCharts.

The Guggenheim fund's largest holding is just 1.15% of assets, so it's clearly diversified across holdings. But it's not as diversified across asset classes. Around 36% of its assets are in high-yield corporate bonds, nearly 32% are in bank loans, and nearly 19% are in asset-backed securities.

A rising rate environment can pressure high-yield corporate debt as better-quality debt is likely to become available as rates rise. Similarly, investors may demand a wider yield spread as high-yield debt is seen as more at risk in a rising rate environment. For example, refinancing could prove to be an issue.

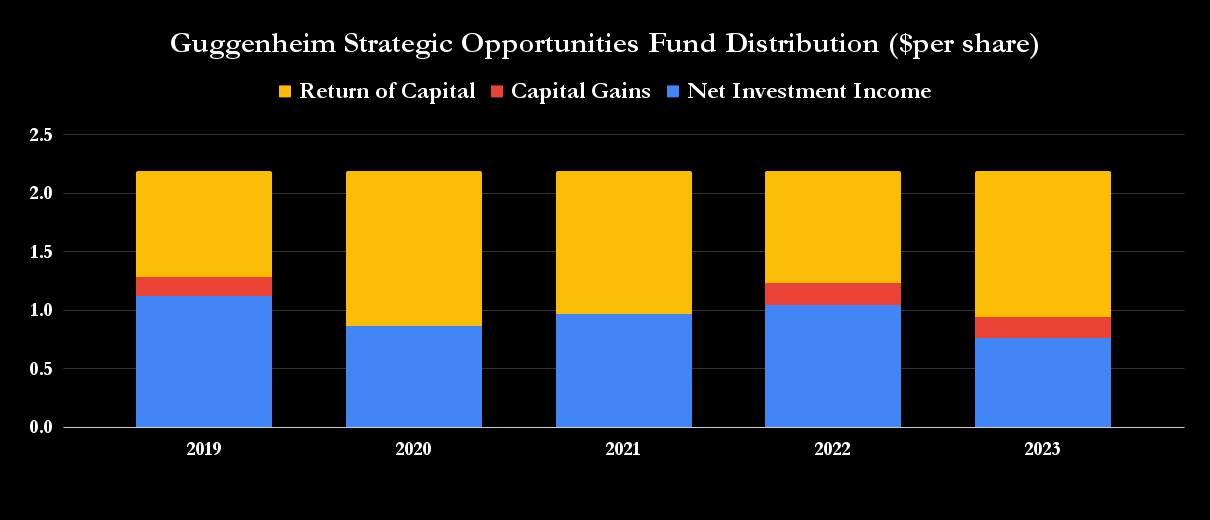

Net-investment income and distributions

As with the Brookfield fund, the Guggenheim fund's distributions have not been covered by net-investment income in recent years. Instead, they have been paid by a combination of net-investment income and return of capital (ROC). The problem of paying distributions out of ROC is it comes from NAV.

The fund has paid a yearly distribution of $2.19 per share for the last seven years. As shown below, less than 35% of last year's distribution came from net-investment income. While there's nothing wrong in returning capital to fundholders through distributions, the decline in NAV (see chart above) over the period suggests it is detrimental to NAV.

Data source: Guggenheim Strategic Opportunities Fund SEC filings.

Using leverage

Finally, let's look at leverage, specifically how the fund has increased borrowing through reverse-repurchase agreements whereby an asset is sold under an agreement to repurchase it at a higher price.

The table shows how the fund has increased its borrowing, and its asset coverage (a measure of how easily it can repay debts by selling assets) has deteriorated; a lower number implies less coverage.

Guggenheim Strategic Opportunities Fund | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|

Total Principal Amount Outstanding (Borrowings) | $0 | $19.3 million | $38.5 million | $128 million | $343.5 million |

Net Assets | $641.8 million | $648.9 million | $878 million | $1,492 million | $1,473 million |

Asset Coverage per $1,000 of Principal Amount | 0 | $34,621 | $23,806 | $12,661 | $5,290 |

Data source: Guggenheim Strategic Opportunities Fund SEC filings.

Understanding the risk

All told, the fund has increased borrowing, while NAV has declined, and its distributions are not covered purely out of investment income. Note that the return of capital portion paid in the distribution ($2.19 per share) in 2023 of $1.25 is equivalent to 10.1% of the current NAV.

As such, the distribution is under considerable threat unless the underlying assets start to appreciate and grow NAV. The premium to NAV that the market is applying to the share price implies that's what the market thinks will happen, but many things need to go right before that occurs.

While the interest rate environment may well turn around for the fund, I don't think the risk/reward calculation justifies buying the stock at this price.

10 stocks we like better than Guggenheim Strategic Opportunities Fund

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Guggenheim Strategic Opportunities Fund wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 28, 2023

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.