Many folks get into investing by following legendary investors like Peter Lynch or Warren Buffett. But no matter what era or style of investor you look up to, chances are a big reason for their success is that they buy hidden gem stocks and let those positions compound over an extended period.

Some investors are famous for buying undervalued companies. Others make a name for themselves by betting on growth trends and having the patience to let technologies pierce into the mainstream.

However, one of the simplest and most underrated investing strategies is to buy a hidden gem dividend stock -- a company that blends a reliable and steadily growing payout with the potential for compound gains. Here's why investors might want to keep an eye on Starbucks(NASDAQ: SBUX), Pentair (NYSE: PNR), and Westlake Chemical Partners LP(NYSE: WLKP).

Image source: Getty Images.

Give your passive income a jolt with Starbucks

Daniel Foelber (Starbucks): Starbucks is one of the most powerful consumer brands in the world. But the quality of the company's dividend is often overlooked.

The company started paying a dividend in 2010. And since then, it has raised its dividend every single year. The raises have been sizable, too. Today, Starbucks pays a $0.53 per share quarterly dividend. In 2017, its dividend was about half of that.

Starbucks doesn't have the highest yield -- just 2.1%. But its commitment to dividend raises, paired with its industry-leading position, means the stock is packed with passive income potential.

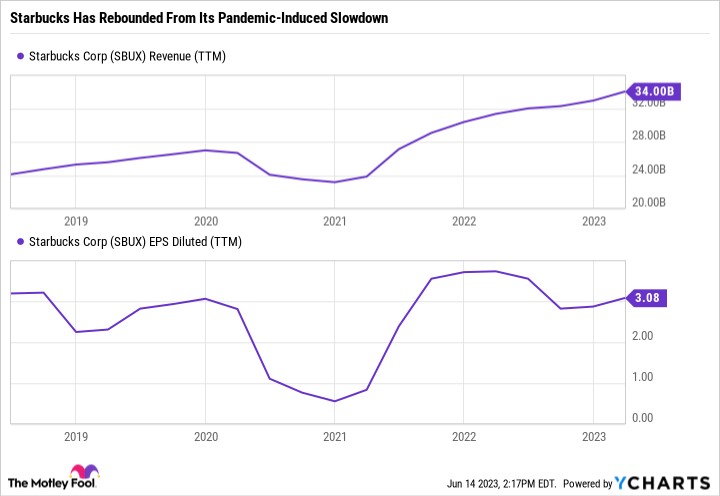

Starbucks has done an excellent job recovering from its COVID-19-induced sales and earnings slowdown. The company's revenue is at an all-time high, and its earnings are back on track to grow at a modest rate.

SBUX Revenue (TTM) data by YCharts. EPS = earnings per share. TTM = trailing 12 months.

Starbucks may not be the scorching hot growth stock it once was. But the company deserves a seat at the table of blue chip dividend stocks. Starbucks generates plenty of free cash flow to cover the dividend. And the company's effective expansion of rewards members and mobile ordering can help boost customer engagement for years to come.

Pentair has room to grow its dividend

Lee Samaha(Pentair): The water solutions company used to be bigger, but its electrical business was spun off as nVent in 2018. Still, that doesn't change that the company has increased its dividend for 47 consecutive years. In addition, the current dividend of $0.88 is very well covered by estimated earnings per share of $3.60 to $3.70 in 2023.

That's not to say that Pentair doesn't face some headwinds. Management's guiding toward full-year sales growth in the range of a decline of 2% to being flat in 2022. The main reason is declining sales in its core pool equipment segment. Pentair was a big winner from pandemic lockdowns in recent years as customers focused on spending money on their homes. However, it's now being hit by a combination of a natural correction in demand and rising interest rates putting pressure on spending.

As CEO John Stauch noted on the second-quarter earnings call, "We've reduced our pool revenue expectations, reflecting both a lower sell-through due to economic uncertainty and the previously expected inventory headwinds."

But here's the thing. Management also raised the low end of its adjusted earnings guidance from $3.50-$3.70 to $3.60-$3.70 due to strength in its non-residential businesses (fluid treatment and commercial water solutions) and an ongoing transformation initiative aimed at cutting costs -- the target is to increase its return on sales, or operating profit margin, from 18.6% in 2022 to 23% by 2025.

Suppose Pentair archives its aims, and its residential business recovers (likely, as there's now a larger installed base of pools in North America) alongside ongoing strength in its non-residential business. In that case, investors could look forward to many more years of dividend growth.

Westlake Chemical Partners provides better passive income through chemistry

Scott Levine (Westlake Chemical Partners): Whether you're on the prowl for a high-yield dividend to strengthen your income portfolio, a quality stock sitting in the bargain bin, or a little of both, Westlake Chemical Partners -- and its 8.6% forward-yielding stock -- should be on your radar.

Approaching its 10-year anniversary on the public markets, Westlake Chemical Partners is a limited partnership formed by Westlake Corporation in 2014 to develop ethylene production assets. With the recent distribution in May, Westlake Chemical Partners has logged 35 consecutive payments to unitholders and grown its distribution by 71% since its first payout in 2014.

Westlake Chemical Partners has three primary assets, including three ethylene production facilities and a 200-mile pipeline in Texas for the transportation of ethylene. The operation of these assets generates strong and steady cash flows that help the company fund its distributions to unitholders. In 2022, for example, Westlake Chemical Partners declared distributions of $66.4 million and generated distributable cash flow of $75.9 million, representing a coverage ratio of 1.14. Similarly, in 2021, Westlake Chemical Partners hadn't jeopardized its financial health to reward unitholders, as it had a distribution coverage ratio of 1.06.

Down about 17% from its 52-week high, units of Westlake Chemical can be scooped up on the cheap. The stock is valued at 1.5 times operating cash flow, representing a discount to its five-year average of 1.9. For income investors seeking a diamond in the rough -- one that doesn't require them to dig deep into their pockets -- Westlake Chemical Partners warrants consideration.

10 stocks we like better than Starbucks

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Starbucks wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 12, 2023

Daniel Foelber has the following options: long July 2023 $95 calls on Starbucks and short July 2023 $97.50 calls on Starbucks. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Starbucks. The Motley Fool has a disclosure policy.