If you're in search of ultra-high yield stocks, then NextEra Energy Partners(NYSE: NEP) has probably popped up on your radar screen. The clean-energy-focused master limited partnership (MLP) has a huge 13.5% distribution yield.

However, yields don't usually get that high without a good reason. Here's why you might want to tread with caution if you're considering buying NextEra Energy Partners.

What is NextEra Energy Partners, really?

On the surface, NextEra Energy Partners is a master limited partnership (MLP) that owns and builds clean energy assets, like solar and wind power. MLPs are pass-through entities designed to create material income streams for unitholders that often allow for the deferral of taxes because things like depreciation "pass through" to unitholders. So it isn't shocking that NextEra Energy Partners has a high yield. However, 13.5% is very high, even for an MLP.

Image source: Getty Images.

This is a bigger problem when you look at NextEra Energy Partners from further back. This MLP was created by utility giant NextEra Energy(NYSE: NEE). Its purpose is to buy clean-energy assets from NextEra Energy via transactions known in the industry as dropdowns. Assuming everything is working as planned, a dropdown is a mutually beneficial deal.

NextEra Energy takes a cash-flow-generating asset and sells it, generating capital that it can use to build a new asset. NextEra Energy Partners issues debt and sells units to afford the purchase but increases the cash flow it generates to support its distributions. This all works out as long as NextEra Energy Partners can sell units and issue debt at attractive levels.

Things have changed for NextEra

You've probably already figured out the problem: With NextEra Energy Partners' yield of 13.5%, it's very expensive for the company to issue new units. On top of that, the high-interest-rate environment over the past couple of years has made it more expensive to issue debt. NextEra Energy Partners isn't as useful as it once was to parent NextEra Energy.

To make matters worse, through the first six months of 2024, NextEra Energy paid distributions of $374 million, while generating cash available for distribution of $384 million. While it's good that it paid out less than it earned, the distributable cash-flow payout ratio is a worryingly high 97%. Another way to look at this is that the distribution was covered by distributable cash flow by a slim 1.03 times. Either way, there isn't much room for adversity.

If something doesn't change, NextEra Energy Partners' very existence starts to become questionable. The easy answer is just to trim the distribution, but that would probably upset the income-focused investors who own the MLP.

It's also possible that NextEra Energy Partners just needs to muddle through for longer until investments start to come online and increase cash flow. Only that doesn't change the long-term picture, since NextEra Energy Partners' real purpose is to provide its parent NextEra Energy with an additional -- and attractive -- source of growth capital.

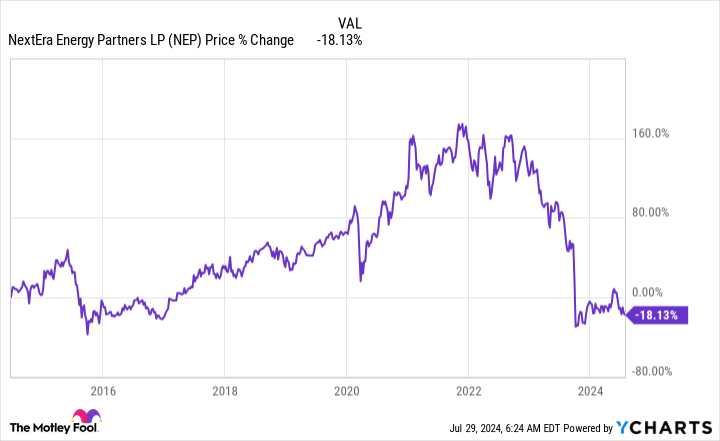

Another option is for NextEra Energy to give up on the whole thing and buy back NextEra Energy Partners. That's not as crazy as it sounds, given that NextEra Energy Partners is currently trading nearly 20% below its initial public offering (IPO) price.

Notably, this is exactly what other utilities did in the pipeline space a few years ago. In this case, NextEra Energy Partners investors would have to find a new home for their cash or share in far-lower-yielding NextEra Energy's stock.

Things could change quickly for NextEra Energy Partners

So far, NextEra Energy has stood behind NextEra Energy Partners, which is good. But if the yield remains elevated, the MLP isn't a valuable funding tool for its parent, and that will eventually force NextEra Energy to make a hard choice.

If you own NextEra Energy Partners for the lofty yield, the high distributable cash-flow payout ratio is a warning sign that the risk is elevated. Watch this investment very closely, or you might end up shocked if the story changes in a not-so-attractive way for income investors.

Should you invest $1,000 in NextEra Energy Partners right now?

Before you buy stock in NextEra Energy Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and NextEra Energy Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $635,614!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends NextEra Energy. The Motley Fool has a disclosure policy.