Who wouldn't want to own an investment with a more than 13% yield that was also in a position to increase its disbursements by 6% a year? I'd think every income investor would consider backing up the truck to load up on such an asset. Given that the average annual return on the stock is around 10%, even growth investors would have to consider buying in.

Those levels of return are what NextEra Energy Partners (NYSE: NEP) is currently offering investors. But don't get too excited. There's trouble in this ultra-high-yield paradise.

The NextEra Energy Partners' backstory

If you look at NextEra Energy Partners in isolation, you'll miss the most important piece of the master limited partnership's (MLP) story. That's because it serves a very specific purpose for its parent, utility giant NextEra Energy(NYSE: NEE). NextEra Energy basically created NextEra Energy Partners for the sole purpose of having an MLP buyer for its renewable power assets. In the industry, these sales are called "drop downs."

The purpose of dropping down assets from NextEra Energy to NextEra Energy Partners is to raise capital at the parent level so NextEra Energy can continue to build more renewable power assets. These aren't one-sided transactions. NextEra Energy Partners taps the capital markets by selling units and issuing bonds so it can pay for the assets that are being dropped down. But in an ideal world, those assets will generate reliable cash flows that more than cover the financing costs, producing additional cash flow that can be distributed to unitholders.

When everything works out as planned, this becomes a virtuous circle and everybody wins. NextEra Energy gets to grow its business using NextEra Energy Partners as a low-cost source of capital. And NextEra Energy Partners wins because its cash flows increase, allowing it to pay growing distributions.

That's the dream, anyway. Things haven't been working out quite as planned lately.

The big problem facing NextEra Energy Partners

In the first quarter, NextEra Energy Partners generated $164 million in distributable cash flow, up from $156 million in the same quarter of 2023. Cash flow growth is good, of course -- but it also paid out $188 million in distributions in Q1, up from $169 million a year ago. That means it is paying out more than it can afford right now, and did a year ago as well. Nor were those quarters one-off cyclical occurrences. For the full year of 2023, the MLP produced $689 million in distributable cash flow but distributed $741 million.

To be fair, MLPs can pay out more than their distributable cash flows for short periods of time. That often happens when they have investments in their pipelines that will eventually generate enough cash flow to close the gap. So, in and of itself, this disparity isn't a death knell for NextEra Energy Partners.

But there's one other worry. Because investors are downbeat on clean energy and interest rates have risen, NextEra Energy Partners' cost of capital has increased.

For example, it just issued a note with a 7.5% coupon so it could pay off a note with a 4.25% coupon. If it chose to raise funds by selling units, that would mean having to support the dividends on those units at more than 13%. With financing costs on the rise, dropping assets down from NextEra Energy to NextEra Energy Partners is not quite as compelling a transaction as it was. This isn't the first time a controlled MLP has faced a dilemma like this -- this exact situation occurred in the pipeline sector a few years ago. Many parent companies resolved those difficulties by buying back their MLP children, often at attractive valuations for the parent.

Be careful with NextEra Energy Partners

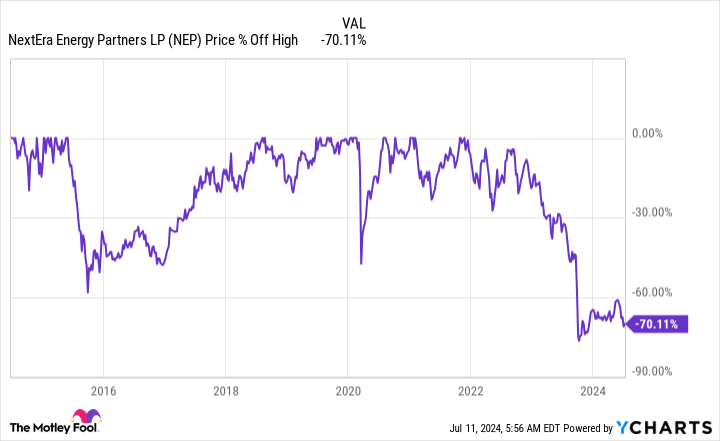

NextEra Energy Partners still has big plans, but those plans are likely to get harder and harder to achieve given the increasingly high cost of capital it faces. The price of its units has fallen 70% from its peak, and they now trade more than 15% below where they were when NextEra Energy created the MLP. Unless there's a dramatic decline in the financing costs that NextEra Energy Partners faces, it is very possible that NextEra Energy will buy back NextEra Energy Partners in the next five years because the MLP just isn't as useful as it was. If that happens, the MLP's investors will likely end up owning shares of NextEra Energy, which has a dividend yield of just 2.8%.

Should you invest $1,000 in NextEra Energy Partners right now?

Before you buy stock in NextEra Energy Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and NextEra Energy Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 8, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends NextEra Energy. The Motley Fool has a disclosure policy.