On Sept. 18, the Federal Reserve lowered the target range for the federal funds rate by a half-percentage point, marking the first rate cut in more than four years.

Lower interest rates can spur capital investment, lower the unemployment rate, and help accelerate economic growth. However, rate cuts have been followed by mixed results in the stock market -- with gains generally occurring when recessions are avoided.

The ripple effects of the rate cut remain to be seen. But the cut should be generally good news for the energy sector, especially exploration and production (E&P) companies like ConocoPhillips(NYSE: COP). Here's why the dividend stock is a buy now.

Image source: Getty Images.

ConocoPhillips' medium-term plan

During the past year, there has been a flurry of mergers and acquisitions (M&A) in the oil patch. ConocoPhillips initially sat on the sidelines before joining the party this spring when it announced a blockbuster deal to buy fellow E&P Marathon Oil. It expects to close the deal in the fourth quarter.

ConocoPhillips expects the combined business to generate so much free cash flow that it can accelerate growth, raise the dividend, and buy back stock. It plans to offset the newly issued equity in the all-stock transaction in two to three years. If successful, ConocoPhillips would emerge as a better business with no dilution to its shareholders or impact on its balance sheet. It's a tall order, but ConocoPhillips has recently returned a ton of capital to shareholders. In 2024 alone, ConocoPhillips plans to distribute at least $9 billion to shareholders through buybacks and dividends.

Benefits of lower interest rates

Higher oil prices can help ConocoPhillips achieve its targets. ConocoPhillips estimates a $120 million to $130 million change in 2024 annualized cash flow per $1 change in the price of West Texas Intermediate (WTI) crude oil (when oil is in the range of $60 to $90 per barrel WTI). So the difference between $70 and $80 crude oil is more than $1 billion in cash flow.

In 2024, ConocoPhillips is targeting full-year capital expenditures of $11.5 billion and operating costs of $9.2 billion to $9.3 billion. The footprint of the business will be even larger once it integrates Marathon Oil.

In sum, ConocoPhillips has sizable operational and financing capital commitments -- namely buybacks, dividends, operating expenses, and capital expenditures. Lower interest rates make borrowing costs cheaper, which allows ConocoPhillips to refinance debt if needed or take on new debt at a lower rate.

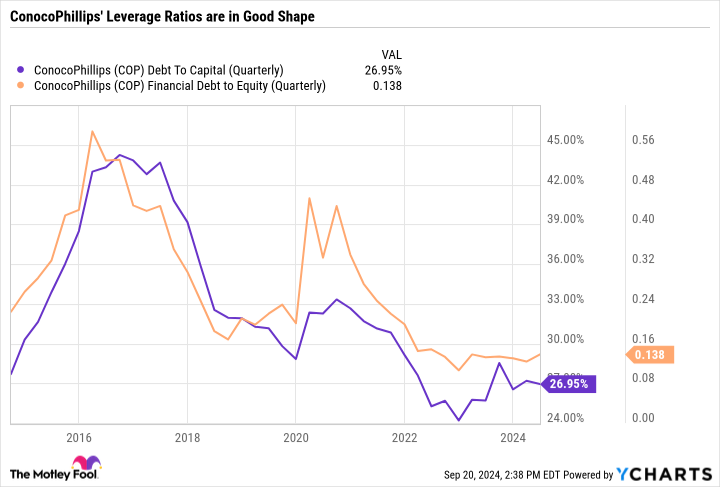

That said, ConocoPhillips prides itself on having a lean balance sheet and low leverage. As you can see in the chart, ConocoPhillips sports a 27% debt-to-capital ratio and a 0.14 debt-to-equity ratio -- both near 10-year lows.

COP Debt To Capital (Quarterly) data by YCharts

The lower the ratios, the less dependent a company's capital structure is on debt. Leverage ratios tend to spike when oil prices fall, which you can see in the aftermath of the 2014 to 2015 oil and gas downturn and the 2020 COVID-19-induced collapse. In this vein, ConocoPhillips' balance sheet is well positioned to endure lower oil prices.

A quality payout

A higher interest rate on risk-free products like a certificate of deposit or high-yield savings account makes dividend stocks comparatively less attractive. When interest rates are high, investors who care more about passive income than potential capital gains may gravitate toward the sure bet rather than endure stock market risks. The reverse is true in a lower interest rate environment.

ConocoPhillips is changing its dividend program to make it more predictable. It used to pay both an ordinary dividend and a variable dividend based on the business's performance. Now, it will fold the variable dividend into the ordinary dividend for a quarterly payment of $0.78 per share -- or an annualized yield of about 2.8%. Based on management's plans, investors can expect the company to prioritize buybacks and gradual increases to the ordinary dividend.

A 2.8% dividend yield isn't necessarily high-yield territory. Still, it's more than double the yield of the S&P 500. The 10-year Treasury rate just reached its lowest level in more than a year and is now 3.7%, about a full percentage point lower than its highest level in 2024. So, ConocoPhillips' dividend is now within striking distance of the risk-free rate.

ConocoPhillips is built to last

Highly leveraged oil and gas companies may boom and bust depending on borrowing costs and oil prices. But ConocoPhillips is a balanced business that positions itself to succeed even if interest rates are relatively high and oil prices are mediocre.

Given the cyclical nature of the oil and gas industry, it is better to choose a company built to endure downturns than to bank on one that can thrive only when the conditions are just right.

ConocoPhillips has a solid dividend and has laid out clear expectations for investors. It remains a top-tier E&P to buy now.

Should you invest $1,000 in ConocoPhillips right now?

Before you buy stock in ConocoPhillips, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ConocoPhillips wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $760,130!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 23, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.