Nvidia(NASDAQ: NVDA) completed its 10-for-1 stock split after market close on Friday, June 7. Like most forward stock splits, this one followed significant share price appreciation. The stock surged 225% during the past year and 850% since November 2022, when the launch of ChatGPT sparked the artificial intelligence (AI) gold rush.

Nvidia remains well-positioned to benefit as more businesses invest in AI. Indeed, it is arguably the best pure-play AI stock. However, stock splits have historically been bad news for Nvidia shareholders. The company's value has declined by an average of 23% during the 12-month period following past splits.

Here's what investors should know.

Historically, stock splits have been bad news for Nvidia shareholders

Excluding the most recent one, Nvidia has completed five stock splits as a public company, and shares have consistently declined afterwards. The chart below details when each stock split took place, and it shows how the stock performed during the next six months, 12 months, and 24 months.

Stock Split Date | 6-Month Return | 12-Month Return | 24-Month Return |

|---|---|---|---|

June 2000 | (50%) | 28% | (52%) |

September 2001 | 44% | (72%) | (49%) |

April 2006 | 63% | 1% | (6%) |

September 2007 | (45%) | (70%) | (53%) |

July 2021 | 30% | (4%) | 145% |

Average | 8% | (23%) | (3%) |

Data source: YCharts.

As shown above, following the last five stock splits, Nvidia returned by an average of 8% during the next six months. But shares declined by an average of 23% during the 12-month period following the split, and the stock was still down by an average of 3% after 24 months. In short, history says Nvidia could suffer a severe drawdown in the not-so-distant future.

Of course, past performance is never a guarantee of future results, and that saying rings particularly true here. Four of the last five stock splits occurred in close proximity to severe bear markets. Specifically, the S&P 500 declined 49% between March 2000 and October 2002 due to the dot-com bubble, and it declined 57% between October 2007 and March 2009 due to the global financial crisis.

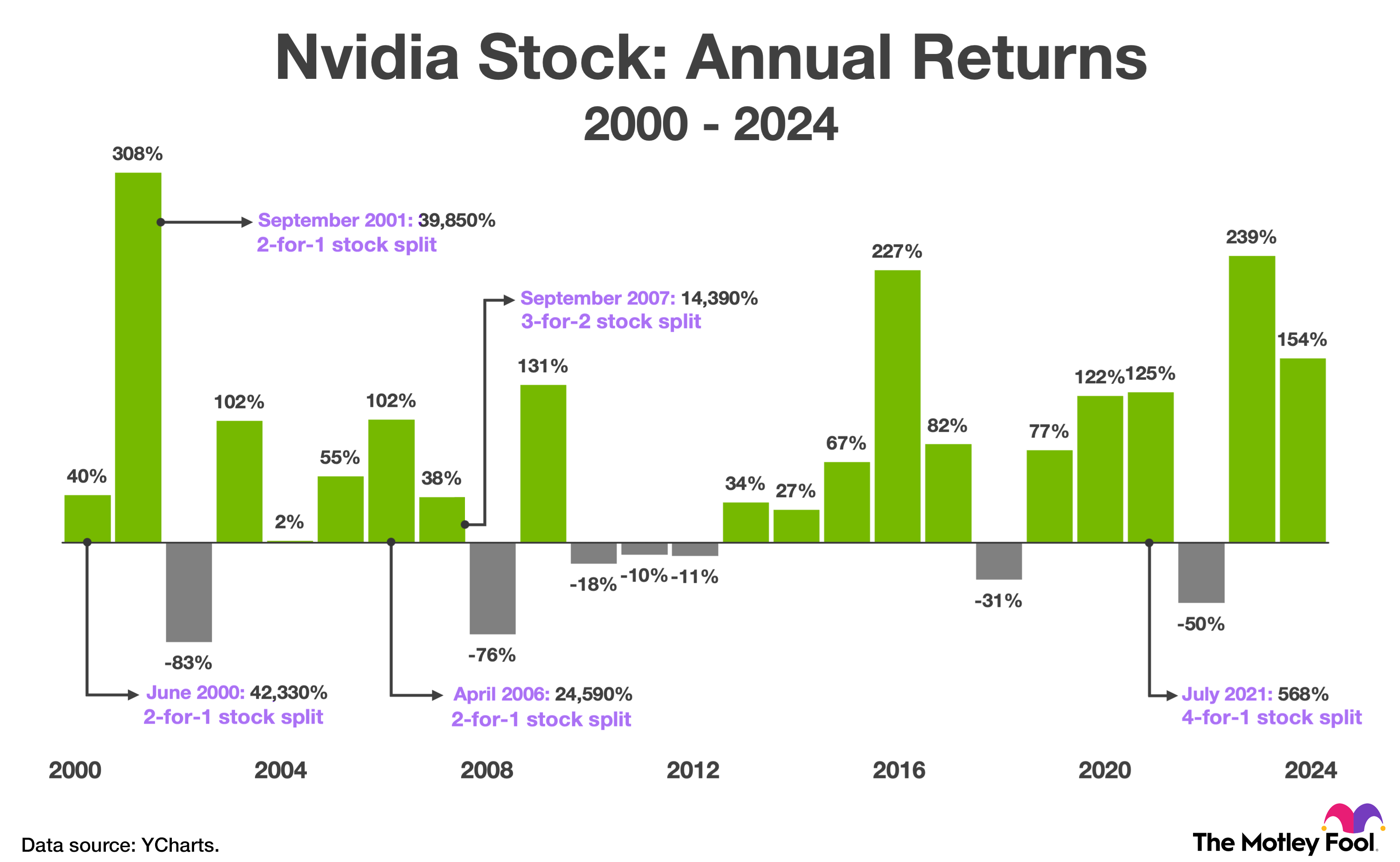

Those market crashes notwithstanding, there has still been a silver lining for patient investors. Nvidia shares ultimately rebounded following all five stock splits and produced phenomenal long-term returns. The chart below shows the magnitude of those returns as of June 12, 2024.

The chart shows Nvidia's annual return between 2000 and 2024, and the total return following each stock split as of June 12, 2024.

Going forward, whether Nvidia is a good or bad investment depends on two things: (1) how quickly the semiconductor company can grow earnings per share, and (2) how much investors are willing to pay for those earnings.

Nvidia has a durable competitive advantage

Nvidia's graphics processing units (GPUs) have a near-monopoly in accelerated computing, a discipline that uses specialized hardware and software to speed up complex data center workloads like artificial intelligence (AI) and data analytics.

Nvidia products consistently set performance records in AI training and inference at the MLPerf benchmarks, standardized tests that provide unbiased evaluations of AI systems. Additionally, the company holds more than 90% market share in data center GPUs and more than 80% market share in AI chips.

Nvidia bears brush aside those strengths and cite mounting competition as cause for alarm. Specifically, they point to semiconductor companies like AMD and cloud providers like Amazon, Microsoft, and Alphabet, all of which are building chips to supplant Nvidia GPUs. But that bearish argument ignores the formidable economic moat Nvidia has in its full-stack strategy.

CEO Jensen Huang recently told analysts: "We literally build the entire data center." He means Nvidia is no mere chipmaker, but rather a full-stack computing company. Nvidia supplements its GPUs with central processing units (CPUs) and networking hardware that's purpose-built for artificial intelligence. The company also offers subscription software and cloud services that support AI workflows across numerous end markets, from manufacturing and logistics to customer service and healthcare.

The heart of Nvidia's full-stack computing platform is CUDA, a parallel programming language that allows GPUs (originally engineered for graphics processing) to function as data center accelerators. The CUDA ecosystem is comprised of hundreds of frameworks and software libraries that streamline the development of complex applications. That gives Nvidia an immense advantage, because no other chipmaker has a comparable ecosystem of supporting software.

To quote Morningstar analyst Brian Colello, "CUDA is proprietary to Nvidia and only runs on its GPUs, and we believe this hardware plus software integration has created high customer switching costs in AI, contributing to Nvidia's wide moat."

Nvidia stock looks a little pricey at its current valuation

Going forward, Wall Street expects Nvidia to grow earnings per share at 31.7% annually over the next three to five years. If that number is divided into its current price-to-earnings multiple of 75.8, the quotient is a price/earnings-to-growth (PEG) ratio of 2.4. That multiple is a discount to the three-year average of 3.2, but it's still relatively pricey on an absolute basis.

That said, the consensus earnings forecast leaves room for upside. Spending on AI hardware, software, and services is forecasted to compound at 36.6% annually through 2030, according to Grand View Research. Nvidia could certainly match that pace, and perhaps exceed it. To that end, its current valuation could appear quite reasonable or even cheap in hindsight.

Ultimately, investors have a somewhat difficult decision here, but I think Joseph Moore at Morgan Stanley has the right idea. "[W]e think the backdrop warrants AI exposure even amid extreme enthusiasm -- and Nvidia remains the clearest way to get that exposure," he wrote in a recent note to clients.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $794,196!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Trevor Jennewine has positions in Amazon and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.