Engaging in hypothetical exercises can be a great way to filter out the noise and focus on your highest-conviction ideas: companies that you believe are worth buying no matter what happens in the stock market through the end of 2025.

Out of the thousands of publicly traded U.S.-based companies, a little more than 50 of them qualify as Dividend Kings, which are companies that have paid and raised their dividends for at least 50 consecutive years. There are plenty of recognizable names on the list, like Procter & Gamble, Coca-Cola, Lowe's Companies, Walmart, Target, and more. Raising a dividend year after year is a testament to financial stability and earnings growth.

But not every Dividend King has what it takes to sustain that dividend growth into the future. A lot of top names pop out when scanning the list. But none shine brighter than PepsiCo (NASDAQ: PEP). Here's why it is a compelling dividend stock to buy now.

Image source: Getty Images.

PepsiCo's strength is its diversification

PepsiCo is a highly diversified food and beverage business. Besides its flagship Pepsi soda brand, it owns a variety of other beverages including Gatorade, Mountain Dew, Ocean Spray, Lipton, Tazo, and more. The company also owns chip and snack giant Frito-Lay -- which encompasses Doritos, Cheetos, Lay's, Ruffles, and dozens of other products -- and Quaker Oats.

The company has a much more diverse product lineup than its peer, Coca-Cola, which doesn't play in the snack food business. The advantage of PepsiCo's strategy is that it can better handle a slowdown in a particular product category. But in some instances, it lacks the pricing power of a more focused company like Coke, which bets big on its best ideas.

In recent years, PepsiCo has faced pricing pressure and declines in sales volume across all its categories. The declines haven't been too drastic, but margins have taken a noticeable hit. However, as you can see in the chart, sales soared from 2020 to 2022, so the company was due for a pause.

PEP revenue (TTM) data by YCharts; TTM = trailing 12 months.

PepsiCo is addressing its challenges

Results haven't been great, but the company has been up-front about its medium-term strategy for driving volume growth. PepsiCo is returning value to customers by increasing the amount of chips and snacks per bag and boosting the quantity of some variety packs.

For example, it is investing in Doritos and Tostitos for the fall football season through bonus bags that have more product and cater to group events. PepsiCo is adding 20% more product in Tostitos and Ruffles bags to drive attention to those brands. The company is also changing its variety-pack strategy by offering 10-count quantities as opposed to 18-count and 24-count.

The balance between product quantity and price varies from product to product. But PepsiCo is showing a clear understanding of what consumers are looking for and how it can address the issue most cost-effectively.

After all, it could keep its offerings the same and cut prices to drive volume growth. But instead, it is giving customers more product -- essentially the opposite of "shrinkflation," a term used to describe decreasing quantity while holding prices steady.

In hindsight, PepsiCo raised prices by too much over the last few years, making many products relatively expensive. It's painfully evident in its results that there is little room for further price increases, which is why management is getting creative.

PepsiCo is doing what it can to address its volume declines. It could also get a boost from a gradual improvement in the economy and consumer spending. It has the characteristics of a company that can turn things around quickly. There's nothing wrong with the product line. Rather, the company just has to get a better handle on presentation and pricing.

PepsiCo is a great value

If PepsiCo stock had gone up in lockstep with the broader market over the last few years, it would probably look overvalued right now, given the company isn't at the top of its game. But the stock price is essentially the same today as it was three years ago.

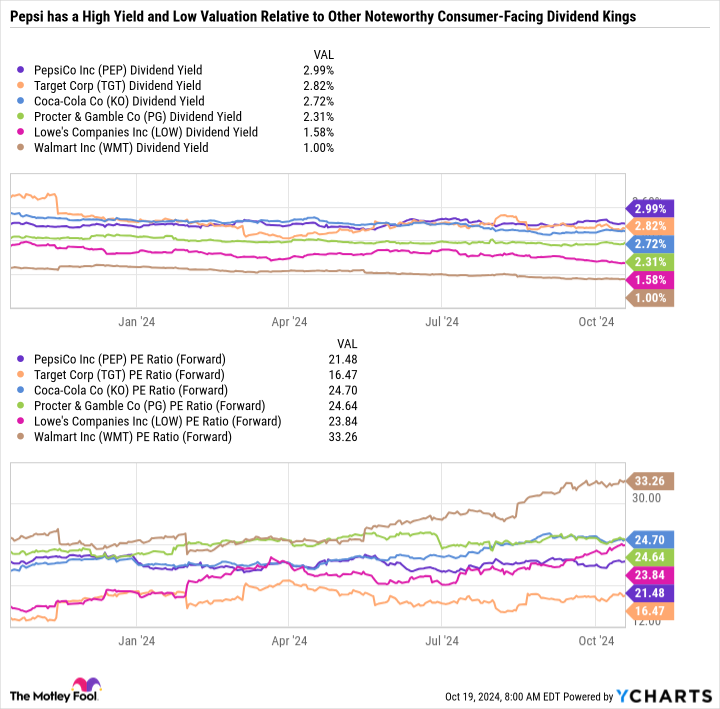

The stagnating price paired with dividend raises and the prospect of earnings growth has pushed the share's dividend yield up to 3% and the forward price-to-earnings ratio (P/E) down to just 21.5. That's a compelling blend of passive income and value, especially compared to other consumer-facing Dividend Kings.

PEP dividend yield; data by YCharts.

As you can see in the chart, PepsiCo and Target have by far the lowest valuations and highest yields of these companies. Target is a solid Dividend King, but it isn't as safe as Pepsi.

Target has a discretionary product mix and can face steep slowdowns as the economy ebbs and flows. It would be a top five Dividend King to buy through 2025, but it's not as compelling as PepsiCo right now.

PepsiCo is the perfect buy-and-hold Dividend King

Sometimes, the best investment thesis is a simple one. PepsiCo hasn't executed well over the last few years but is laying the groundwork to make up for its mistakes. The stock is a great value with a generous yield and should be able to continue growing its dividend by the mid-single digits per year.

In sum, it is everything you should want from a Dividend King: reliability, passive income, not overpaying from a valuation perspective, and the ability to raise the dividend even during economic slowdowns. PepsiCo has these qualities in spades, making it a top safe stock to buy now.

Should you invest $1,000 in PepsiCo right now?

Before you buy stock in PepsiCo, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PepsiCo wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $879,935!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 21, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Target and Walmart. The Motley Fool recommends Lowe's Companies. The Motley Fool has a disclosure policy.