As the old saying goes, the stock market is a staircase up and an elevator down. In plainer terms, gains tend to compound gradually over time, while sell-offs can happen in a heartbeat.

That's certainly been the case for Johnson Controls(NYSE: JCI), Li-Cycle Holdings(NYSE: LICY), and Enphase Energy(NASDAQ: ENPH) which are down 14.1%, 25%, and 15.3%, respectively, in the past month.

Despite the sell-off, all three companies are chock-full of long-term potential. Here's why each growth stock is worth buying now.

Image source: Getty Images.

Management deserves the benefit of the doubt

Lee Samaha(Johnson Controls): The long-term future for Johnson Controls looks bright. The heating, ventilation, air conditioning, building controls, and fire and security products company helps increase building efficiency, which is important since buildings are major emitters of carbon dioxide. Meeting net-zero commitments is a goal this company can help others reach.

Moreover, its digitally connected solutions are significantly increasing the value-add to its offerings. Buildings are getting smarter and more efficient, and Johnson Controls is at the heart of the movement.

Unfortunately, the company disappointed investors by recently downgrading its full-year 2023 sales guidance. The reason? In short, dealers are electing to run down inventory rather than take delivery of products. The market's worried about this because it's the typical sort of behavior that presages a drop in end demand. In other words, dealers see demand weaken and pause taking delivery of products from Johnson Controls.

That may be the case here, too, but some context is needed. An alternative view argues that the reality is the supply chain crisis -- which hit Johnson Controls and made it challenging to deliver certain products in 2022 -- caused dealers to rush to build up inventory as soon as it became available. As such, they are now running down inventory as lead times ease.

Management thinks the sales slowdown is temporary and indicates as evidence the ongoing strength in orders for building solutions -- equipment, installation, and services.

I think management's argument is plausible, and the company continues to report high single-digit growth in field orders and double-digit year-over-year growth in building solutions services orders -- a sign that the digital initiatives are gaining traction.

I think the dip in the share price following the third-quarter earnings report is creating a good buying opportunity in a long-term growth stock.

Li-Cycle is a battery stock that's bound to bounce higher

Scott Levine (Li-Cycle Holdings): After soaring more than 27% through the first two months of 2023, shares of lithium-ion battery recycler Li-Cycle Holdings failed to maintain the upward trajectory and have subsequently headed in the opposite direction, falling more than 26% over the past six months. One of the main culprits for the stock's recent decline was a disappointing financial report in which the company reported Q2 2023 revenue and net income that failed to meet analysts' expectations. Despite this recent setback, the company reported several achievements that suggest the stock can certainly charge higher in the months ahead.

Li-Cycle's operations rely on two types of facilities: spokes and hubs. At the spoke facilities, Li-Cycle processes used lithium-ion batteries into a product called black mass; afterward, the company sends the black mass to hub facilities, where it's processed into battery-grade metals: lithium, cobalt, and nickel.

For a growth stock like Li-Cycle, the recent volatility is certainly understandable, but it belies the company's successes. On Aug. 1, for example, Li-Cycle commenced operations at its spoke facility in Germany, where it now can process 10,000 metric tons of lithium-ion batteries (LIBs) annually, and the company expects to expand operations in the second half of 2023 to result in annual processing capacity of 30,000 metric tons. For context, Li-Cycle had annual LIB process capacity of 51,000 metric tons before the start of operations in Germany. Elsewhere in Europe,, Li-Cycle is developing spoke facilities in Norway and France.

With demand for lithium, nickel, and cobalt expected to rise in concert with the increasing demand for lithium-ion batteries, Li-Cycle offers a compelling opportunity -- one that investors can take advantage of now, with the stock having retreated from its highs earlier in the year.

Dark clouds for Enphase Energy

Daniel Foelber (Enphase Energy): It's been a terrible year for solar stocks. The Invesco Solar ETF(NYSEMKT: TAN), which tracks the performance of the solar industry, is down 33% over the past year and 18.3% year to date despite what has been an excellent year for growth stocks.

Enphase Energy has been the poster child of the sell-off. The microinverter and solar system provider stock is at a two-year low after reporting worse-than-expected guidance during its recent earnings call.

Enphase is now the worst-performing Nasdaq 100 stock. However, context is in order.

Enphase was one of the best-performing stocks from 2020 up to the end of 2022. The stock reached a nosebleed valuation. And the only way to justify its high price was sustained growth, which Enphase failed to deliver.

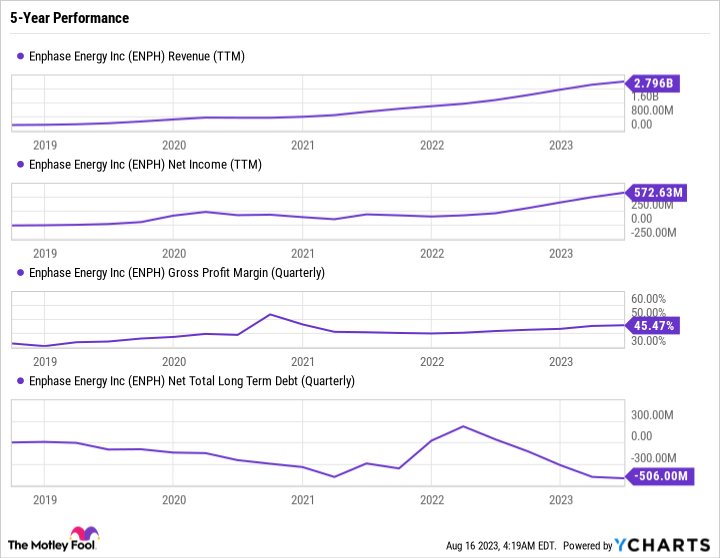

The good news is that Enphase's results on their own are excellent. Enphase has incredibly high gross margins for a company that sells a physical product. It also has a net cash position on its balance sheet. And its trailing-12-month revenue and net income are still up big time compared to past years.

ENPH Revenue (TTM) data by YCharts

Management has done an excellent job branching out to provide more than just microinverters, which gives Enphase more control over other elements of residential solar and small-scale commercial solar offerings. Having more control of the system instead of proving a single component is a way to retain high margins and garner more business.

Enphase is a great company in a cyclical industry. And unfortunately, it all came crashing down at the wrong time because Enphase stock was overvalued heading into the current industry downturn.

Enphase stock could keep falling further from here. But good companies are able to persevere through difficult times. For investors who believe in Enphase's products and management's long-term growth strategy, now is the time to take a hard look at buying the stock.

10 stocks we like better than Johnson Controls

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Johnson Controls wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 28, 2023

Daniel Foelber has positions in Enphase Energy and has the following options: long November 2023 $195 calls on Enphase Energy, long September 2023 $135 calls on Enphase Energy, short November 2023 $200 calls on Enphase Energy, and short September 2023 $140 calls on Enphase Energy. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Enphase Energy. The Motley Fool has a disclosure policy.