Everyone knows it's been a rough year on Wall Street. Major indexes like the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average are likely to close out 2022 in the red.

Yet, there is a stock that has delivered a 26% year-to-date return, and, better yet, it's poised to repeat that performance in 2023. The stock is Deere & Company(NYSE: DE), and here's why it's a no-brainer buy heading into the new year.

Image source: Getty Images.

Deere just turned in a stellar year

Many companies have struggled in 2022. And there are good reasons why. Inflation is high, the Federal Reserve is hiking interest rates, and the U.S. dollar's rise has put foreign exchange pressure on large multinationals based in the U.S. Yet, Deere has shrugged off these headwinds and delivered an absolute home run of a year.

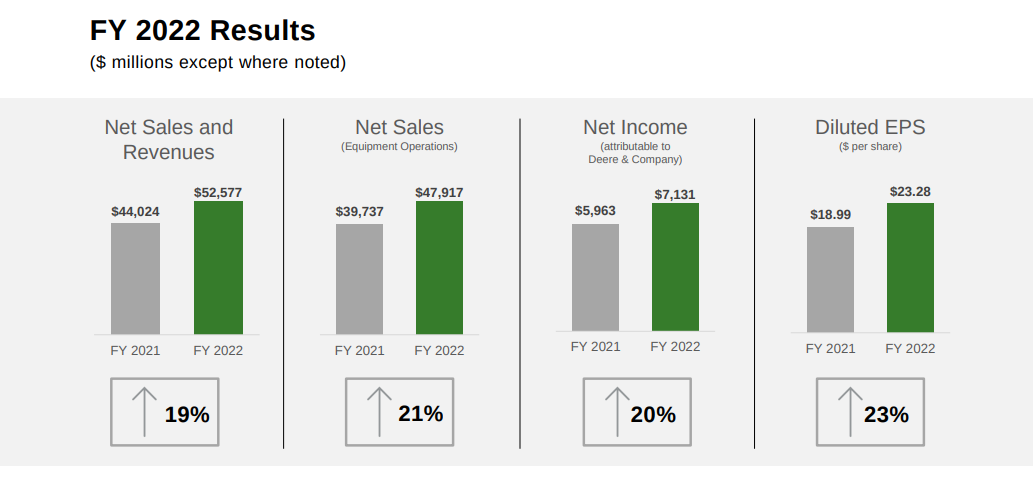

Image source: Deere & Company Investor Relations.

As you can see above, Deere grew sales by 19% year over year. Net income surged 20% to $7.1 billion; earnings jumped 23% to $23.28/share. Simply put, Deere had a historic year. In its most recent quarter (the three months ended Oct. 29, 2022), Deere recorded quarterly revenue growth of 43%. That's its highest level since the 1980s.

To say the company's management is executing its strategy is an understatement. Deere is firing on all cylinders.

Deere's pricing power is leading to industry-best margins

Running a farm is hard. You need lots of land, good weather, know-how, and some very expensive machinery. For example, take combines, the machines used to harvest grains. A new one often costs $1 million or more.

Over the last year, as commodity prices have swung wildly due to supply chain issues and the conflict in Ukraine, many farmers have invested in new machinery to help meet the growing demand for agricultural products. And Deere, with its trusted brand status, has hiked its prices in response.

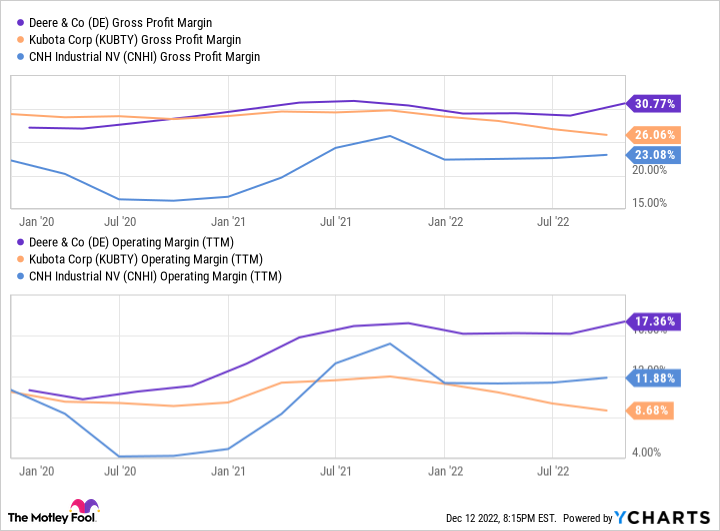

DE Gross Profit Margin data by YCharts

In turn, Deere's margins have expanded. The company boasts gross and operating margins that dwarf its nearest competitors Kubota Corporation and CNH Industrial NV.

Is Deere a buy now?

As impressive as Deere's performance in 2022, I think 2023 (and beyond) will be even better. The company is likely to benefit from ongoing tailwinds from order backlogs for its equipment and increased purchases due to last year's infrastructure package.

Wall Street analysts agree and are bullish on Deere. They expect the company to earn $28.05/share in 2023, up 20% year over year. And those estimates have been rising. Only 90 days ago, Wall Street expected Deere to earn $26.14/share, demonstrating how quickly earnings estimates can change after a company delivers a blowout quarter.

That's not to say Deere is a sure thing. The global economy is still fragile, and a recession in 2023 isn't out of the question. However, for me, Deere is a no-brainer stock that investors can buy and hold -- knowing that it is a well-run and well-positioned company committed to delivering value for shareholders for years into the future.

10 stocks we like better than Deere

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Deere wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2022

Jake Lerch has no position in any of the stocks mentioned. The Motley Fool recommends Deere. The Motley Fool has a disclosure policy.