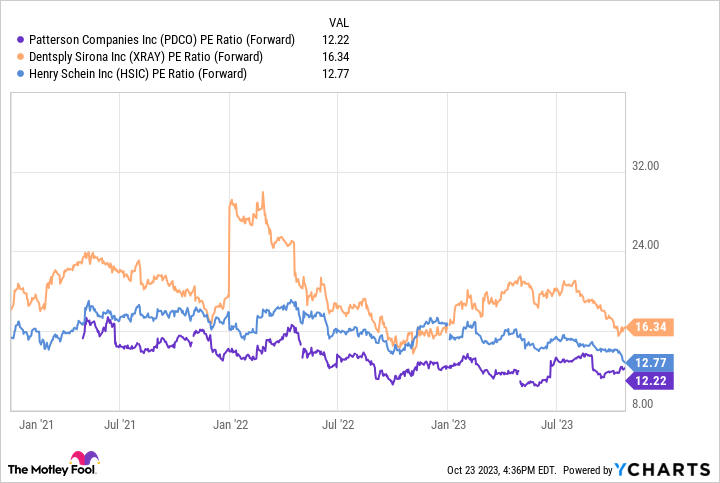

Like regular flossing, dental supply companies are sometimes overlooked, but Henry Schein(NASDAQ: HSIC), Dentsply Sirona(NASDAQ: XRAY), and Patterson Companies(NASDAQ: PDCO) are all thriving, thanks to margin-improvement initiatives in the industry and a rebound from pandemic-related restrictions. The stocks appear to be reasonably priced with forward price-to-earnings ratios below 17.

Those aren't the only reasons to be bullish on these three healthcare stocks. Demographic trends toward an older population, an increased demand for cosmetic dentistry, and increased rates of periodontal disease due to poor diets all point toward growth in the global dental market. According to a report by Fortune Business Insights, the market's size is expected to grow from $38.21 billion in 2023 to $65.23 billion by 2030.

PDCO PE Ratio (Forward) data by YCharts

1. Size, scope give Henry Schein an edge

Henry Schein has been in business for 90 years. It distributes dental and medical products for office practices in 33 countries, and it leads North America, Europe, Australia, New Zealand, and Brazil in dental product distribution sales. Since going public in 1995, the company has a 12.1% compound annual growth rate (CAGR) in annual sales, plus a 13.5% CAGR in annual earnings per share (EPS).

The company's size gives it certain economies of scale and it has been quite active in mergers and acquisitions to foster growth. It just wrapped up its purchase of private medical products company Shield Healthcare for an undisclosed amount. In April, it completed its majority share purchase of Biotech Dental, known for its practice management software solutions, for $423 million. And in May, it signed a deal to buy S.I.N. Implant System, an implant maker from Brazil, for an undisclosed amount.

In the second quarter, the company reported revenue of $3.1 billion, up 2.3% year over year, despite a decrease of $96 million in COVID-19-related personal protection equipment revenue. The company's net income fell by 12.5% year over year to $140 million, and its EPS was $1.06, down 8% compared to the same period last year. The drop in both is connected to the company's purchase of Shield Healthcare for an undisclosed amount, which it completed in the quarter. Even with the drop, the company maintained its yearly revenue guidance of 1% to 3% revenue growth over 2022.

The stock is down more than 15% this year, but considering that it has grown revenue for five consecutive years and said it expects to do so again this year, it may be underpriced at a forward price-to-earnings ratio of 12.22.

2. Dentsply Sirona is building a bridge to the future

Dentsply Sirona is a dental equipment manufacturer and dental consumables producer that markets its products in more than 120 countries. The company saw both revenue and EPS growth in the second quarter and recently raised its full-year sales and adjusted EPS guidance, but its shares are up less than 2% to start this year.

In the second quarter, the company reported revenue of $1.03 billion, up 0.5% year over year. Net income was $86 million, up 17% compared to the same period last year and EPS rose 17.6% year over year to $0.40. The company operates in five segments: connected technology solutions, essential dental solutions, orthodontic and implant solutions, and Wellspect HealthCare. The one faring the best is orthodontic and implant solutions, which saw sales rise 1.9% year over year, thanks mainly to double-digit growth in aligner sales.

The earnings report prompted the company to raise annual sales guidance by $75 million at the midpoint, to a range of between $3.98 billion and $4.02 billion. The company also boosted yearly adjusted EPS to a range of $1.92 to $2.02, up from an earlier forecast of between $1.80 and $2.

The company has a quarterly dividend, which it raised by 12% this year to $0.14 and it delivers a yield of around 1.73%, slightly more than the S&P 500 average dividend yield of 1.62%. The company has raised its dividend for five consecutive years.

3. Consumables driving Patterson's revenue push

Patterson Companies operates in two segments: dental and animal health. The company's stock is up more than 8% so far this year. Over the past 10 years, it has increased annual revenue by 80.51% and annual EPS by 7.61%.

Having two distinct sales areas helps Patterson because spending on dental health and animal health are both expected to rise in the coming years. A report by the American Pet Products Association puts the likely spending on pets at $143.6 billion in 2023, up from $90.8 billion in 2018.

In the first quarter of fiscal 2024, the company reported revenue of $1.6 billion, up 3.5% year over year, with the growth of consumable products driving both segments. The company's reorganization efforts seem to be paying off because EPS grew even faster, at 25% over the prior year, to $0.32. The company also allayed investor concerns by keeping its full-year EPS guidance of between $2.14 to $2.24.

Patterson has an above-average quarterly dividend with a current yield of around 3.4%. The company raised the quarterly dividend by 4% in 2021 to $0.26 and has kept it there for the past couple of years.

10 stocks we like better than Henry Schein

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Henry Schein wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of October 23, 2023

Jim Halley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.