The past three months have been forgettable ones for the stock market. The S&P 500 is now down more than 6% from its July peak, which is disheartening to say the least.

As veteran investors can attest, however, it's always darkest before the dawn. In other words, as uncomfortable as it might be to do so, now's the time to go fishing for new picks. Here are three ideas to get you started on the search effort before we move too deep into November.

U.S. Bancorp

It's been a tough year for most banks. Although higher interest rates raise profit margins on lending, they also pose the risk of crimping demand for loans and higher credit losses. The Mortgage Bankers Association reports September's demand for home loans reached a 27-year low. October's numbers aren't apt to hint at a recovery either.

Rising interest rates also exposed another alarming problem for the banking business. Although higher rates only pushed a handful of banks like Silicon Valley Bank and First Republic Bank into insolvency, their collapses exposed the fact that most banks' asset bases aren't quite as liquid as investors had hoped. Plenty of major banking entities have seen customers take their money elsewhere, reducing these banks' overall deposits. Never even mind the adverse impact rising interest rates have on economic growth, which also works against banks' bottom lines.

A few smaller, regional banks have mostly sidestepped the bulk of this drama, however. U.S. Bancorp(NYSE: USB) is one of them. Its total deposits are up as of the third quarter, from $497 billion as of Q2 to $512 billion now. And, while the size of its loan portfolio fell just a bit between the second and third quarters, at $377 billion it's still up 12% from a year ago. While net profit fell from the third quarter of 2022, all of that drop stems from more spending on marketing and business expenses that had been decidedly subdued during and because of the COVID-19 pandemic.

Perhaps the most compelling argument for stepping into U.S. Bancorp shares here, however, is how well its loan portfolio's performance is holding up despite the rickety economic backdrop. Last quarter's charge-off ratio of 0.44% of its loans is not only relatively low, but actually fell from Q2's figure of 0.67%.

U.S. Bancorp shares aren't doing great this year, declining 22% and failing to reflect any of the underlying company's resiliency. But don't be discouraged. Newcomers will be buying it while the well-protected dividend is yielding 6% of the stock's current price, and they can get the shares for less than 8 times next year's projected per-share profit of $4.05.

Alphabet

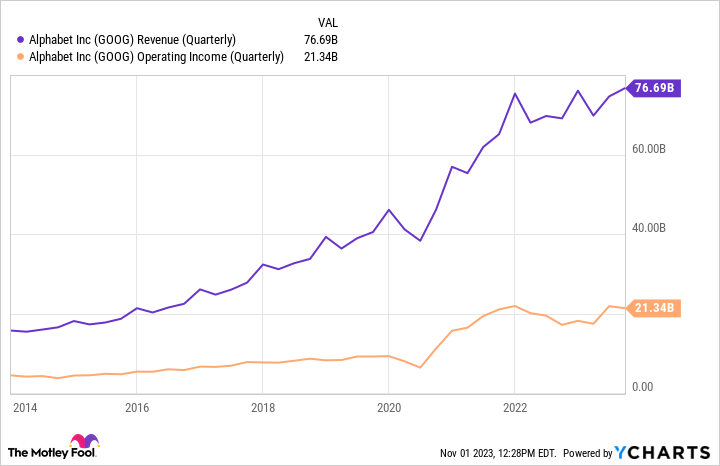

Yes, Google parent Alphabet(NASDAQ: GOOG)(NASDAQ: GOOGL) saw its cloud computing revenue come up short of estimates last quarter. Analysts were calling for cloud sales of $8.62 billion for the three-month stretch ended in September. But the company's cloud arm only did $8.41 billion worth of business. Alphabet shares were hit pretty hard as a result.

This is a case where investors may be losing sight of the bigger picture, however.

Led by its search engine's raw growth, Alphabet's ad revenue was up by more than 9% for the quarter in question, while the entirety of Google's advertising business's operating income rose nearly 27% year over year. And this strength is materializing in an environment where most companies are looking to cut costs when and where they can. They're still spending on search-based ads, suggesting this form of advertising still offers Google's ad clients lots of bang for their buck. That's likely to remain the case for the foreseeable future, extending Alphabet's well-established sales and earnings growth trend. After all, advertising still accounts for about three-fourths of the company's business.

Data source: YCharts

That said, investors may be overlooking a key point about Alphabet's cloud business anyway. Although it didn't generate the sales investors were expecting it to, Google Cloud's top line was still up 22% year over year, and it's still in the black after swinging to a profit in the first quarter of this year. Moreover, on a dollar basis, Alphabet's cloud arm is growing just as much as it ever has. Numbers from Synergy Research Group further indicate Google Cloud is also still gaining market share in this challenging environment, which speaks volumes about how strong its cloud business really is.

Adyen

Last but not least, add payment-processing technology outfit Adyen(OTC: ADYE.Y) to your list of top stocks to buy in November.

Don't sweat it if you've never heard of it. Plenty of North American investors haven't. That's because the Amsterdam-based company does most of its business outside of the U.S., with the bulk of its U.S. business limited to San Francisco and New York. Europe is, unsurprisingly, its biggest market.

Also don't let that lack of familiarity deter you. The payment intermediary is growing like crazy overseas, not to mention growing pretty well in the U.S. despite its relatively small footprint. Revenue rose 21% year over year in the first half of 2023, extending a well-established growth streak. Analysts are calling for comparable sales growth all the way through 2027, as the company continues to disrupt the payments-processing market with better technologies.

But how? At first blush Adyen looks a lot like PayPal or Block, and there are similarities to those companies to be sure. Adyen's arguably got more to offer, however. For instance, it's able to help brands issue their own physical payments cards, identify potential payment fraud, and authenticate a client's own customers when a payment is being made. It's even one of the first fintech names to be certified by the U.S. Federal Reserve to plug into the FedNow instant payment platform, opening the door to new growth opportunities within the U.S.

Whereas PayPal and Block are built from the ground up to serve the consumer first, Adyen's focus is on merchants and their needs. Building its solutions from this vantage point makes a world of difference in terms of its marketability.

The stock's been a fairly poor performer of late thanks to its recent sales shortfall. Take a step back and look at the bigger picture, though. Its overall growth pace remains nothing short of incredible. Its future remains just as bright, making the recent weakness a buying opportunity.

10 stocks we like better than U.S. Bancorp

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and U.S. Bancorp wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of October 30, 2023

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Adyen, Alphabet, Block, PayPal, and U.S. Bancorp. The Motley Fool recommends the following options: short December 2023 $67.50 puts on PayPal. The Motley Fool has a disclosure policy.