Earlier this year struggles at SVB Financial's Silicon Valley Bank and Signature Bank had investors and depositors concerned about the state of the industry. Since then, a couple of other banks have gone down, including the second-largest bank failure ever at First Republic Bank.

While things seem to have calmed down, the risks aren't gone. That's according to Moody's, one of the largest credit raters in the world. On Aug. 7, Moody's downgraded 10 banks and put several others on notice. The ratings firm cited growing financial strains that could hurt these banks' profitability. Read on to see the 10 impacted banks, along with why Moody's decided to downgrade them.

Image source: Getty Images.

Here are the 10 banks Moody's downgraded

Moody's downgraded the credit ratings of 10 small and midsize regional banks across the U.S. following these banks' second-quarter earnings announcements. One concern of Moody's stems from the current economic conditions, which could weigh on these banks' earnings in the near term. Here are the 10 banks Moody's downgraded:

- Commerce Bancshares (NASDAQ: CBSH)

- BOK Financial (NASDAQ: BOKF)

- Old National Bancorp (NASDAQ: ONB)

- M&T Bank (NYSE: MTB)

- Webster Financial (NYSE: WBS)

- Fulton Financial (NASDAQ: FULT)

- Pinnacle Financial Partners (NASDAQ: PNFP)

- Associated Banc-Corp (NYSE: ASB)

- Amarillo National Bancorp (Not publicly traded)

- Prosperity Bancshares (NYSE: PB)

Higher interest rates are weighing on regional banks

In early 2021, inflation, as measured by the year-over-year change in the consumer price index (CPI), rose well above the Federal Reserve's 2% inflation target. While many experts had hoped the inflation would be transitory, it stayed stubbornly high into 2022, prompting the Fed to take action.

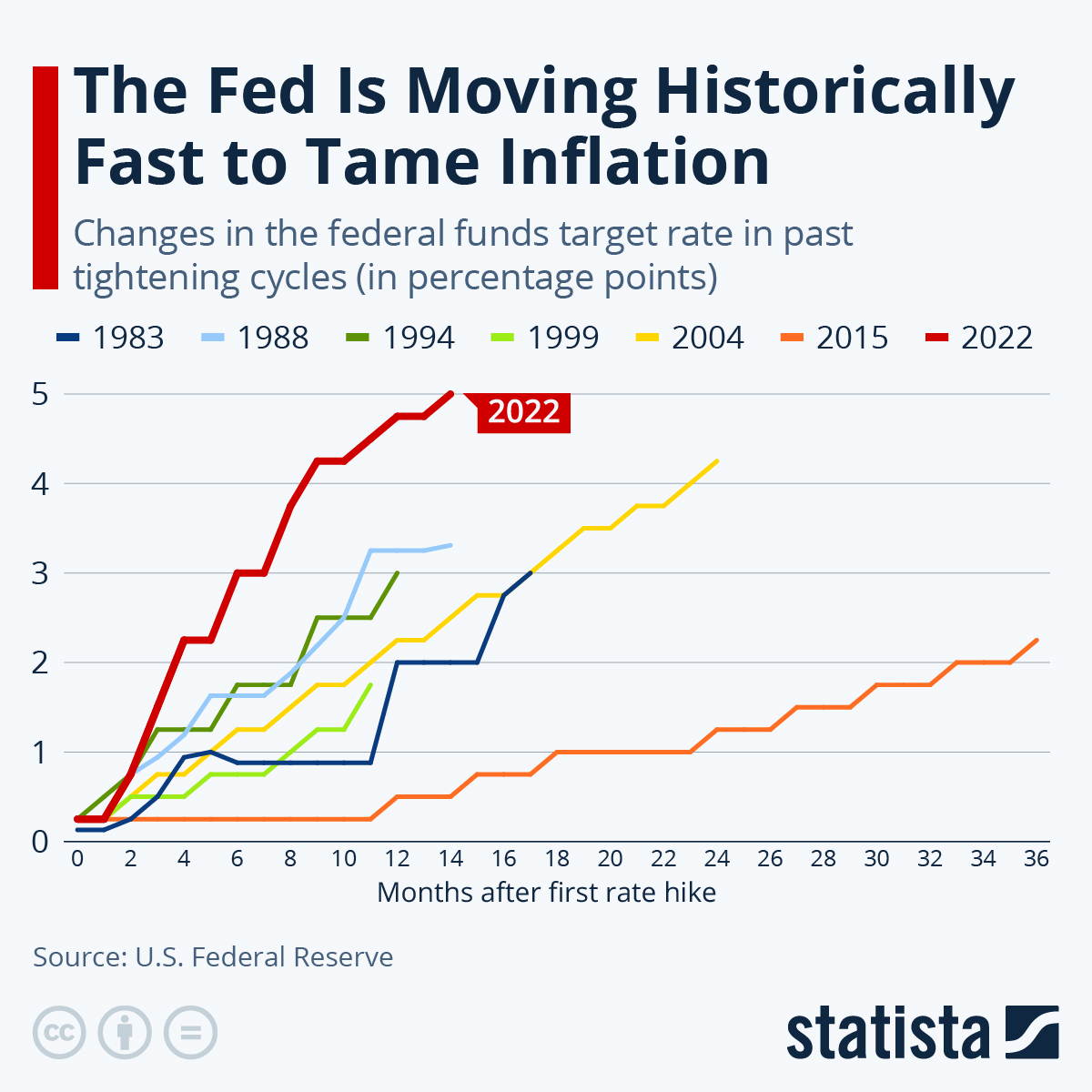

The Fed's primary tool to fight inflation is short-term interest rates. The idea is that higher interest rates restrict borrowing and spending, which reduces demand and helps damp inflation. Since March 2022, the Fed has raised its benchmark interest rate from near-zero to an upper limit of 5.5%.

This pace of interest rate hikes is one of the fastest in more than four decades and has caught some banks off guard. Silicon Valley Bank was the first victim of the higher interest rates. The bank that catered to start-ups saw a huge influx of deposits during the pandemic. From 2020 through 2022, its average deposit base went from $72 billion to over $173 billion-- a 140% change in just two years.

The bank put a lot of this money into long-term bonds, many of which were at ultra-low interest rates due to the environment at that time. Because there is an inverse relationship between interest rates and the value of those bonds, the rapid rise in interest rates drove down the value of the bank's holdings.

Typically this isn't a problem if the bank can hold those securities long-term. However, Silicon Valley Bank faced a perfect storm of problems. Its start-up customers weren't receiving the same levels of funding and they needed to withdraw cash from the bank to stay afloat. In addition, many of the bank's deposits were above the Federal Deposit Insurance Corp.'s $250,000 guaranteed limit. This created a panic among its customers, who raced to pull funds from the bank early this year. The bank sold some of its holdings at a $1.8 billion loss and would've had to sell even more securities at a sizable loss to cover those outflows, eating away at its capital and risking insolvency.

Regulators worried this could spiral out of control and seized the bank. Since then, the Fed introduced the Bank Term Funding Program to shore up liquidity for other banks facing funding issues.

Commercial real estate stress could also weigh on small banks

Higher interest rates have also added stress to the commercial real estate market. Commercial real estate loans are typically made on five- or 10-year terms with a balloon payment at the end. Rather than making the balloon payment, companies tend to extend and refinance these loans at the prevailing market interest rates.

Companies are constantly refinancing their debt, which generally hasn't been a problem over the past decade and a half when interest rates have been ultra-low. However, interest rates are now near their highest in 20 years, resulting in higher costs to refinance these commercial real estate loans. According to data from the Mortgage Bankers Association, 16% of commercial real estate loans mature in 2023, with another 15% maturing in 2024.

In addition, dynamics have shifted in some parts of commercial real estate, like office space. The pandemic brought on more work-from-home or hybrid-work arrangements. Not only that, but many companies have been downsizing for the better part of the past year, resulting in tepid demand for real estate in some major U.S. markets. Banks have also begun tightening lending to those riskier pockets of commercial real estate after the collapse of Silicon Valley Bank in March.

This is a problem for smaller banks because they hold a significant amount of the commercial real estate debt outstanding. According to a report by Goldman Sachs, small banks (those domestically chartered and not among the 25 largest banks) hold 67% of all commercial real estate loans outstanding.

Approach regional banks with caution

Banks have faced pressure from declining deposit balances and falling values of the assets on their balance sheets. Moody's downgrades were primarily related to this and how it could affect smaller regional banks, which have low regulatory capital set aside compared to their larger counterparts.

The stress in the banking system could continue as long as interest rates remain as high as they are. According to CME Group's FedWatch Tool, market participants believe the Fed will hold interest rates near their current levels well into the first half of next year as they look to bring inflation down to the central bank's 2% target.

For those reasons, I'd avoid those regional bank stocks until there is more clarity about the state of the economy, inflation, and the easing of the Fed's aggressive interest rate policy.

10 stocks we like better than Walmart

When our analyst team has an investing tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Walmart wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of MM/DD/YYYY

SVB Financial provides credit and banking services to The Motley Fool. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Goldman Sachs Group and Moody's. The Motley Fool recommends CME Group. The Motley Fool has a disclosure policy.