Since the start of 2020, Ally Financial(NYSE: ALLY) has weathered the pandemic-induced shutdowns, a boom in auto lending, rapidly rising car prices, and recent volatility in the banking sector after the failure of SVB Financial's Silicon Valley Bank and First Republic Bank in recent months.

It should come as no surprise that the stock has had its ups and downs over the years. Ally Financial stock has taken investors on a roller-coaster ride. If you invested $2,000 in Ally Financial at the start of 2020, your investment would have dipped to $770 during the March 2020 sell-off, only to surge higher to $3,834 by early 2021. Today, that initial investment would be worth about $2,065.

Data source: YCharts

Here's how the company has weathered recent events affecting the banking industry and what investors will want to pay attention to next.

Tight automotive inventory levels benefited Ally in 2021

Ally Financial offers customers various financial products and services, including banking, brokerage, credit cards, and loans. However, its roots are in making auto loans. That's because the company was founded in 1919 as the General Motors Acceptance Corp. (GMAC), rebranded as Ally Financial in 2010, and went public in 2014.

In 2020, supply chain disruptions affected everything from inventory to auto production. As a result, there was a shortage of vehicles for sale while, at the same time, demand for vehicles ramped up. Car prices rose, and Ally Financial benefited in a big way.

In 2021, Ally's revenue from its automotive lending business jumped 22%, while its net income blasted 163% higher. It posted stellar margins, but that surge was short-lived. Last year Ally's auto lending business saw revenue grow 1%, net income fell 34%, and margins shrank.

Falling car prices and high interest rates are a drag on the business

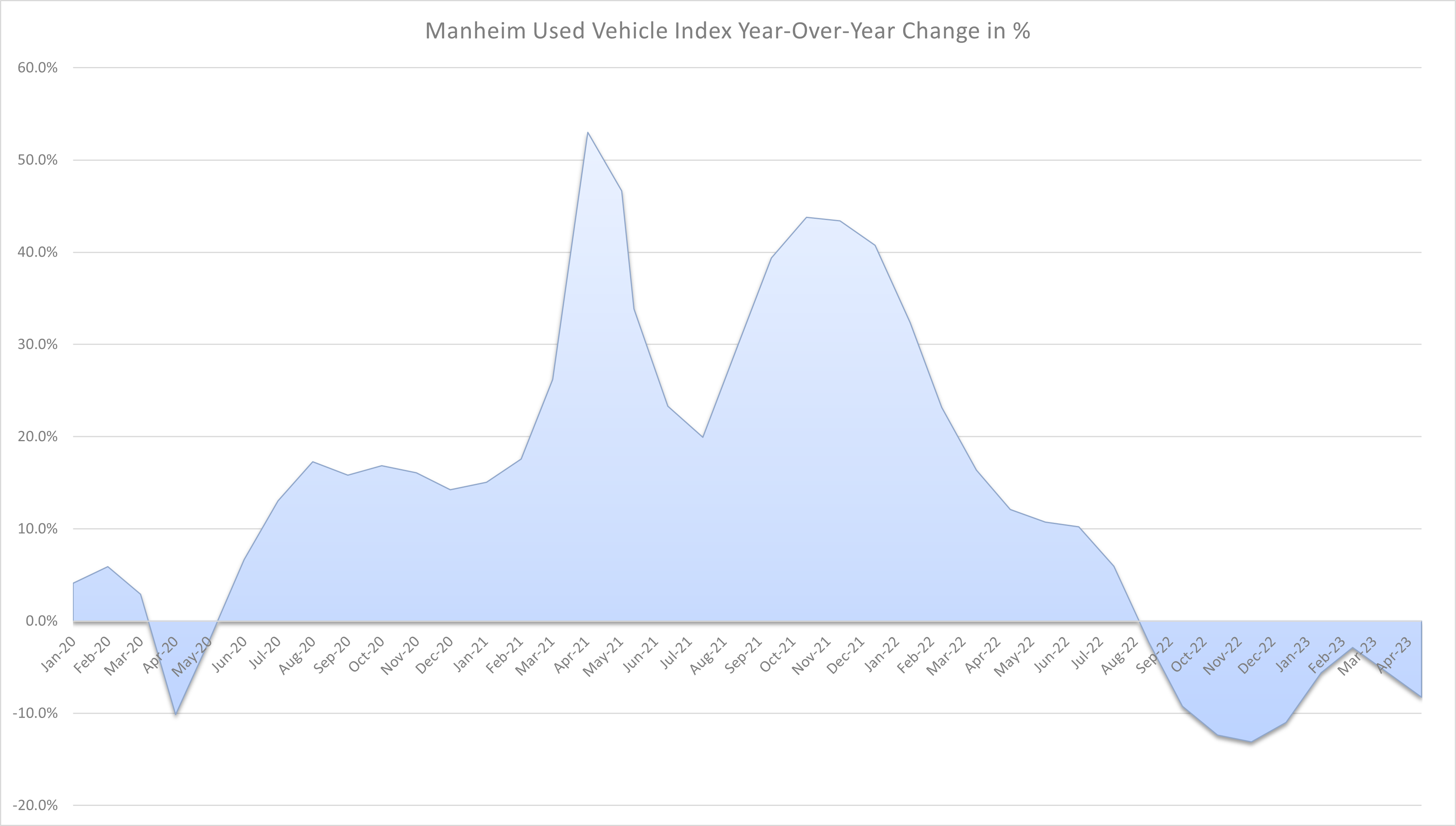

The Manheim Used Vehicle Value Index, which measure the cost of used-vehicle prices, surged from mid-2020 through mid-2022. Since then, the price of used vehicles has fallen year over year every month since September.

Data source: Manheim Used Vehicle Value Index. Chart by author.

Ally's business has struggled with the return to normalcy in the automotive market. The Federal Reserve is raising interest rates in its fight to bring down inflation, which had increased to its highest level in four decades. As a result, the federal funds rate, or the overnight lending rate for banks, went from near-zero to 5.25% in a little over a year.

This has raised the cost of financing anything from mortgages to used cars. When you consider the cost of used vehicles is falling, it appears that the rising interest rates are having an impact on slowing the pace of inflation. However, this has hurt Ally's business, which saw its first-quarter net income fall 51% from the same quarter last year.

Here are the risks you'll want to consider

Ally Financial doesn't face many of the risks that plagued Silicon Valley Bank or First Republic. Ally's deposits grew to $138.5 billion in the first quarter, up $2.5 billion from the prior year and up $800 million from Q4. Also, 91% of its retail deposits are insured by the Federal Deposit Insurance Corp. In comparison, only 15% of Silicon Valley Bank's deposits were FDIC insured.

While Ally doesn't face those deposit flight risks like Silicon Valley Bank, it does have some risks relating to its auto lending business.

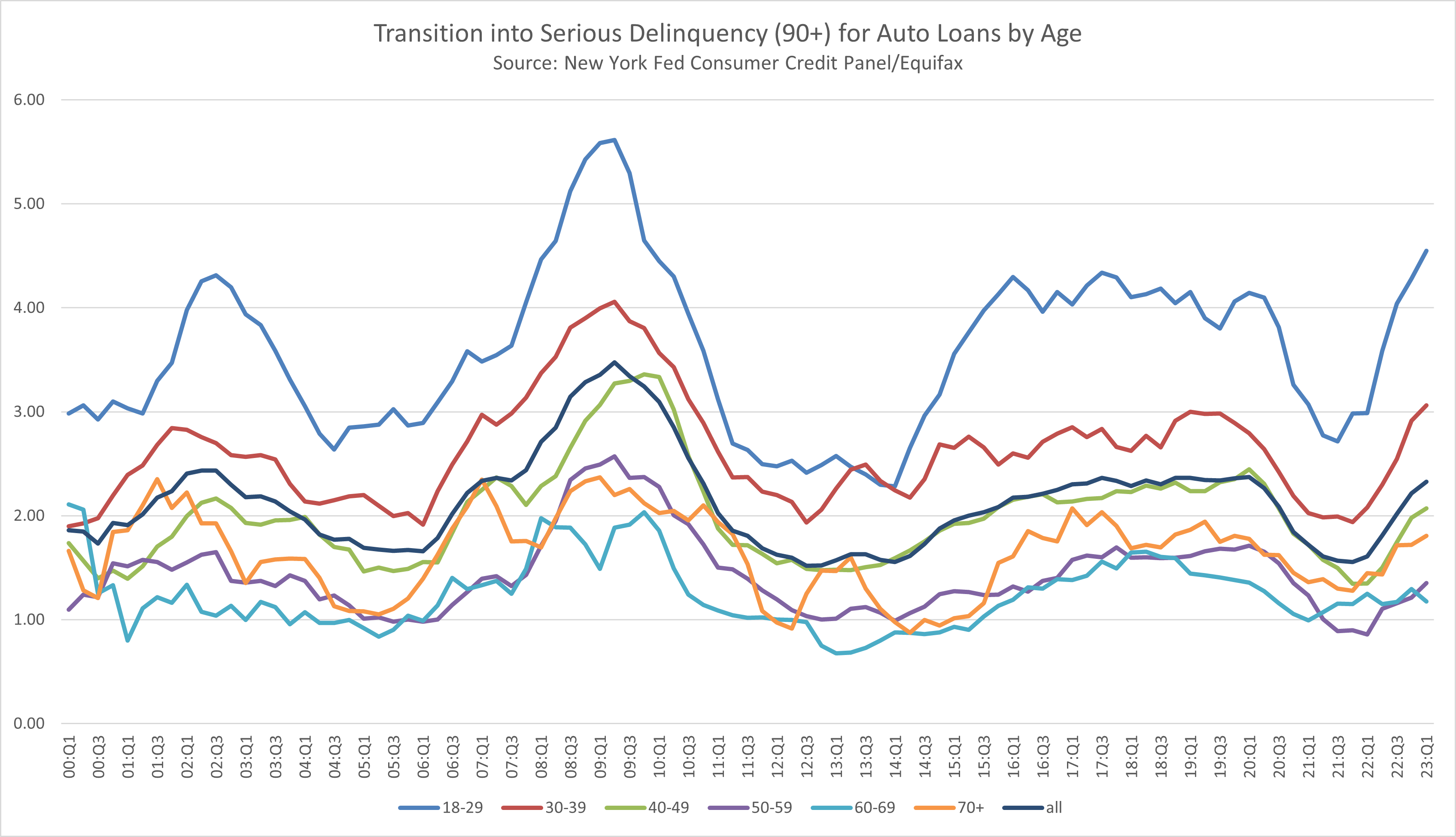

According to the New York Federal Reserve Bank, auto loan delinquencies are rising. Specifically, younger borrowers are getting hit the hardest. According to the Fed, 4.6% of auto loans among borrowers under 30 are in "serious delinquency," the highest level recorded since the Great Recession

Data source: New York Federal Reserve Bank. Chart by author.

In Q1, Ally saw a net charge-off rate of 1.7% on its consumer auto loan portfolio. It also has an allowance for loan losses of $3 billion on its nearly $84 billion auto loan portfolio, or about 3.6%. If it does see defaults continue to tick up, it could be forced to build up more reserves and charge off more loans, which would hurt the bottom line.

Short-term risks could be present an excellent buying opportunity

The biggest short-term risks for Ally are tightening lending conditions and a potentially slowing economy. Entering the year, four out of five economists believed the U.S. could enter a recession in the next two years. Analysts at JPMorgan Chase say the odds of a recession before the end of this year are over 50%. If the U.S. enters a recession, Ally's earnings will continue to take a hit, while defaults on its auto loans could continue to rise.

Ally has done a solid job of consistently increasing its deposits and expanding its offerings. While a recession could weigh on the stock in the short term, a sizable decline in the share price from here could be an excellent buying opportunity for long-term investors.

10 stocks we like better than Ally Financial

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Ally Financial wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 12, 2023

JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. Ally is an advertising partner of The Ascent, a Motley Fool company. SVB Financial provides credit and banking services to The Motley Fool. Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool recommends General Motors and SVB Financial and recommends the following options: long January 2025 $25 calls on General Motors. The Motley Fool has a disclosure policy.