There's a lot of uncertainty around whether or not 2023 will see the U.S. enter into an official recession. Inflation remains at decade-high levels despite multiple large interest rate hikes made by the Federal Reserve this year. The worries and responses point to 2023 being another volatile year for investors.

The good news is that there are stocks well positioned for unstoppable growth in 2023, regardless of what the broader market may be doing. Two real estate investment trust (REIT) stocks that look particularly teed up for another strong year are Iron Mountain(NYSE: IRM) and Farmland Partners(NYSE: FPI).

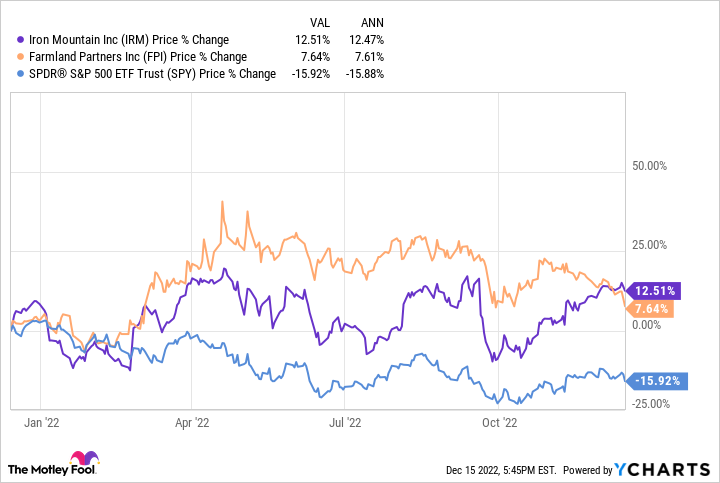

Their stocks are up 12% and 8% respectively over the past year, while the S&P 500 is down nearly 16%. Here's a closer look at these two unstoppable REITs and why they have what it takes to keep growing.

1. Iron Mountain

Iron Mountain works with over 225,000 customers across the globe, helping them organize, digitize, and safely store digital and physical assets. The company started out as a safe and secure way to store things like art, collectibles, or documents during the Cold War era of the 1950s.

Over the years, the company has grown notably. It now owns over 1,300 physical data center storage facilities, as well as 17 data center properties. It offers a slew of online services like document scanning and workflow automation, inventory management, and cloud-based data management.

Iron Mountain had an incredible 2022. The company achieved its highest earnings before interest, taxes, depreciation, and amortization (EBITDA) on record in the third quarter. Its revenue grew by 14% compared to last year, while its adjusted funds from operations (AFFO), a key metric that illustrates a REIT's profitability, rose by 9%. Leasing momentum remains incredibly strong for the company in both its legacy assets, which include physical assets and services, and its data center facilities.

Its strong performance and resilient business model in a challenging economic environment have garnered a lot of attention from investors. The stock is up close to 13% this year and up 43% over the past five years. Year to date, it's already achieved an 18% increase in revenue compared to last year. So its lofty goal of achieving a 10% compounded annual growth rate (CAGR) by 2026 is certainly achievable.

Data center and physical storage demand is a necessity-based service. Many of Iron Mountain's clients need secure digital storage, or may even be required by law to store certain assets in a secure place. This helps reduce Iron Mountain's susceptibility to the effects of an economic slowdown while having lasting demand for decades to come.

Aside from doubling the annualized return of the S&P 500 over the past 25 years, the stock also pays an attractive dividend yield of 4.6% right now -- almost triple the S&P 500 average.

2. Farmland Partners

Farmland Partners is the largest publicly traded agricultural REIT in the market today. It owns roughly 191,000 acres of farmland across 19 U.S. states, leasing it to a network of farmers who grow traditional farm commodities like corn, soy, wheat, rice, and cotton, along with other food and specialized products like nuts, berries, citrus, and avocados.

Farmland Partners hasn't been a huge winner historically. Since it went public in 2014, the stock has only provided a 2.84% annualized return, compared to the 11% annualized return for the S&P 500 during that same period.

However, its lack of growth wasn't necessarily due to its business model, which is actually quite resilient. It was, rather, a result of poor management choices and an expensive battle against a short seller in 2018. Now that the lawsuit is behind it and it's made some changes within its management team, it's seeing much stronger earnings.

Its third-quarter 2022 earnings beat analysts' estimates, with operating income growing by over 200% since last year. The REIT acquired farmland management company Murray Wise Associates (MWA) last year, unlocking a new revenue stream, earning a fee for executing leases between third-party tenants and farmland owners, and helping buy or sell land for farmers. It's now growing this arm of its business heavily while also continuing to buy more land.

The REIT currently trades around 46 times its projected full-year FFO, which is richly valued. The higher price is what's keeping me from personally investing in the stock. However, I do feel it's set to keep growing in 2023. As of November 2022, food costs were up 10.6% since last year, according to the Consumer Price Index (CPI). Food is an essential part of living, so even if food costs keep soaring, demand for it will remain steady. There's also a growing shortage of arable land, making farmland not just one of the most sought-after asset classes today, but a valuable asset for the next century.

The company has made some changes to its dividend payout structure to help it conserve cash and fuel further growth, which puts its yield around 1.9% today, a bit higher than the S&P 500 average.

10 stocks we like better than Iron Mountain

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Iron Mountain wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2022

Liz Brumer-Smith has positions in Iron Mountain. The Motley Fool has positions in and recommends Farmland Partners and Iron Mountain. The Motley Fool has a disclosure policy.