To say the past year has been rough for investors in Ginkgo Bioworks(NYSE: DNA) would be an understatement of the highest order. As of Aug 14, shares of the synthetic-biology stock were down by 86% in 2024.

A beaten-down price isn't the only way the stock market has signaled low expectations. Ginkgo stock has been trading at a steeply negative enterprise value.

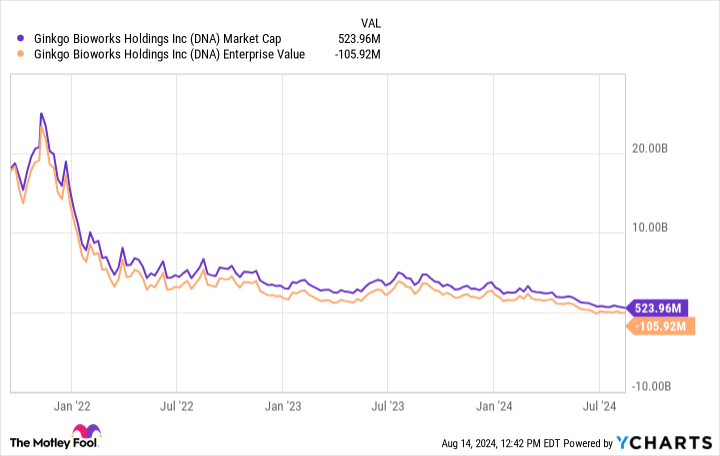

It's a debt-free company that finished June with $730 million in cash and cash equivalents. The stock has been beaten down so severely, though, that you could buy every outstanding share for just $524 million at recent prices.

DNA market cap data by YCharts.

Paying less than cash for a cutting-edge life science business seems like a terrific bargain. Then again, stocks generally don't trade at negative enterprise values unless investors have a good reason to expect steep losses.

Let's measure reasons to buy Ginkgo against reasons to avoid the stock to see if it's a bargain at its beaten-down price.

How Ginkgo stock could outperform

Ginkgo Bioworks is at the forefront of the burgeoning synthetic biology market. Other companies hire it to breed new microorganisms such as yeast and bacteria that produce high-value ingredients, such as novel therapeutics, food ingredients, and chemicals traditionally derived from petroleum.

The company's automated foundry is lowering costs associated with engineering new organisms. Lower foundry costs aren't the only advantage Ginkgo has over potential competitors. It accumulates data every time it operates its foundry. Over time, it can mine its data trove for insights that make its operations even more efficient.

It hasn't been able to make ends meet yet, but a reduction in staff will trim expenses. In June, the company began laying off 35% of its workforce, which should begin reducing operating expenses by about $85 million annually by the end of 2026.

Ginkgo began 18 new cell-engineering programs in the second quarter. Those contracts vary but most include downstream revenue opportunities. Not every program will succeed, but milestone payments and royalties from just a few could drive total revenue to new heights.

Why the stock is falling

Shares of Ginkgo Bioworks have been tanking because the business is bleeding money like a fast-growing start-up that's trying to gain market share. The losses wouldn't be such a problem if its business were growing rapidly, but the opposite is happening.

In the first half of 2024, Ginkgo reported total revenue that sank 42% year over year. Total operating expenses decreased, but not by nearly enough, and the company lost a whopping $383 million in the first half.

A staff reduction is the right move, but it's like using a Band-Aid on a gunshot wound. At its present cash burn rate, Ginkgo will need to ask investors for more capital long before its latest staff reduction achieves the projected $85 million in annualized savings.

A bargain now?

The stock has been beaten down to a negative enterprise value, but it's only a bargain if you expect it to quit bleeding money and turn a profit soon. Unfortunately, this doesn't seem likely.

Ginkgo was founded in 2008 and as of June 30, it had completed 129 programs in addition to 140 that it was running. If its foundry were truly valuable to the clients that hired it, there would be heaps of milestone payments and royalty revenue to report.

Sadly, royalties still don't account for a material amount of total revenue. Moreover, the company hasn't reported any milestone payments this year.

Recently, management began removing downstream value share from certain program types. This looks like a step in the right direction that could lead to more predictable cash flows, but it doesn't make the business a wise investment yet.

Ginkgo Bioworks stock might seem like a bargain with its negative enterprise value, but it isn't. Regardless of your risk tolerance, this stock is best avoided until its bottom line crosses into positive territory.

Should you invest $1,000 in Ginkgo Bioworks right now?

Before you buy stock in Ginkgo Bioworks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Ginkgo Bioworks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $711,657!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. TheStock Advisorservice has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 12, 2024

Cory Renauer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.