Campbell Soup (NYSE:CPB) Posts Q2 Sales In Line With Estimates

Packaged food company Campbell Soup (NASDAQ:CPB) reported results in line with analysts' expectations in Q2 FY2024, with revenue down 1.2% year on year to $2.46 billion. Its non-GAAP profit of $0.80 per share was flat year on year.

Is now the time to buy Campbell Soup? Find out by accessing our full research report, it's free.

Campbell Soup (CPB) Q2 FY2024 Highlights:

- Revenue: $2.46 billion vs analyst estimates of $2.44 billion (small beat)

- EPS (non-GAAP): $0.80 vs analyst estimates of $0.77 (3.9% beat)

- Free Cash Flow of $390 million, up from $31 million in the previous quarter

- Gross Margin (GAAP): 31.6%, up from 30.5% in the same quarter last year

- Organic Revenue was down 1% year on year

- Sales Volumes were down 2% year on year

- Market Capitalization: $12.8 billion

With its iconic canned soup as its cornerstone product, Campbell Soup (NASDAQ:CPB) is a packaged food company with an illustrious portfolio of brands.

Packaged Food

Packaged food stocks are considered resilient investments because people always need to eat. These companies therefore can enjoy consistent demand as long as they stay on top of changing consumer preferences. But consumer preferences can be a double-edged sword, as companies that aren't at the front of trends such as health and wellness and natural ingredients can fall behind. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

Campbell Soup is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 1.1% over the last three years was weak as consumers bought less of its products. We'll explore what this means in the "Volume Growth" section.

This quarter, Campbell Soup reported a rather uninspiring 1.2% year-on-year revenue decline to $2.46 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 1.7% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

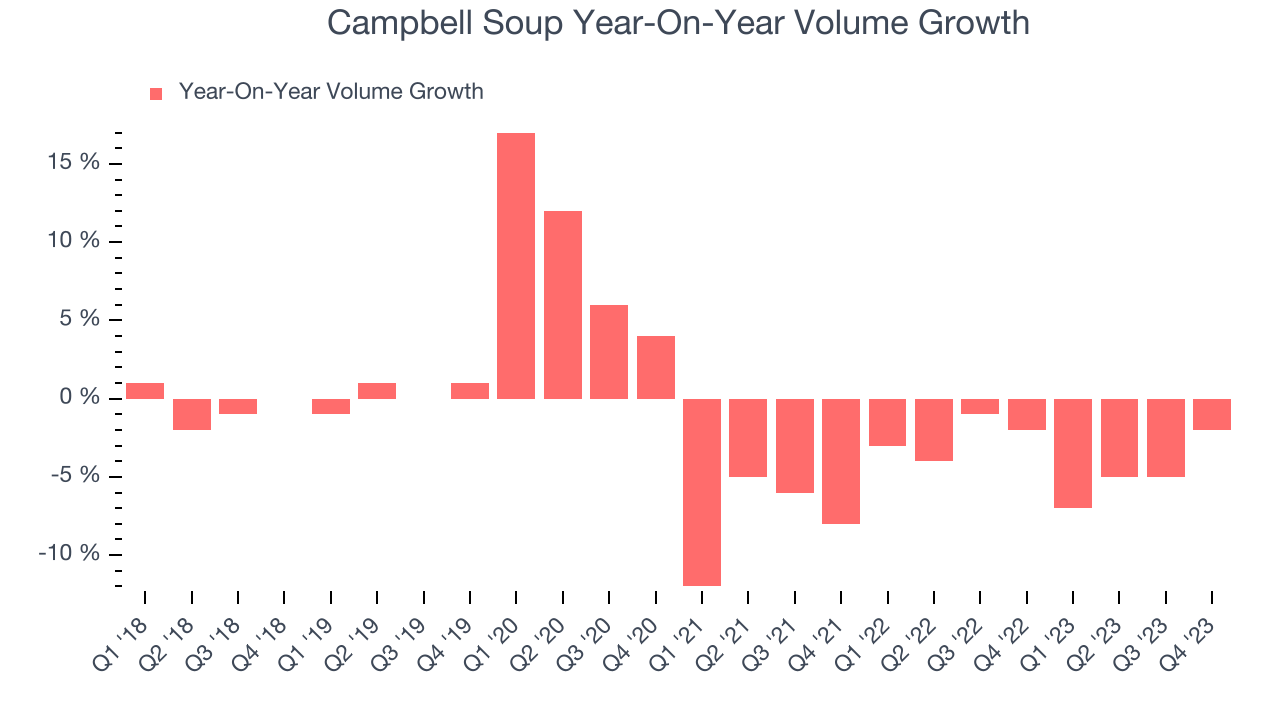

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Campbell Soup generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Campbell Soup's average quarterly sales volumes have shrunk by 3.6%. This decrease isn't ideal as the quantity demanded for consumer staples products is typically stable. Luckily, Campbell Soup was able to offset fewer customers purchasing its products by charging higher prices, enabling it to generate 6.4% average organic revenue growth. We hope the company can grow its volumes soon, however, as consistent price increases (on top of inflation) aren't sustainable over the long term unless the business is really really special.

In Campbell Soup's Q2 2024, sales volumes dropped 2% year on year. This result was a further deceleration from the 2% year-on-year decline it posted 12 months ago, showing the business is struggling to push its products.

Key Takeaways from Campbell Soup's Q2 Results

It was great to see Campbell Soup beat analysts' EPS expectations this quarter, though its sales volumes declined (albeit to a lesser extent than forecasted by Wall Street). With its lower volumes, the company's full-year 2024 revenue guidance fell short, but its full-year EPS guidance exceeded estimates.

Furthermore, Cambell Soup's pending acquisition of Sovos Brands is expected to close the week of March 11th and is not currently baked into its outlook. Sovos Brands' products include Rao's Homemade pasta sauce and Noosa Yoghurt.

Overall, this quarter's results were mixed as its sales were weak but its earnings were better than expected. The stock is flat after reporting and trades at $43.15 per share.

So should you invest in Campbell Soup right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.