Devon Energy(NYSE: DVN) launched a pioneering capital return framework following its transformational merger with WPX Energy in early 2021. It established the industry's first fixed-plus-variable dividend policy. The framework featured a fixed base quarterly dividend and a variable dividend of up to 50% of its free cash flow.

Several oil stocks have since taken a page from Devon Energy's playbook by launching similar fixed-plus-variable dividend policies, including Chord Energy(NASDAQ: CHRD). That oil producer is now taking another page out of Devon's playbook by agreeing to acquire Enerplus(NYSE: ERF), a company Devon had also offered to buy. Here's a look at how the deal will benefit dividend investors and where Devon might turn next to fuel its payout.

Drilling down into the deal

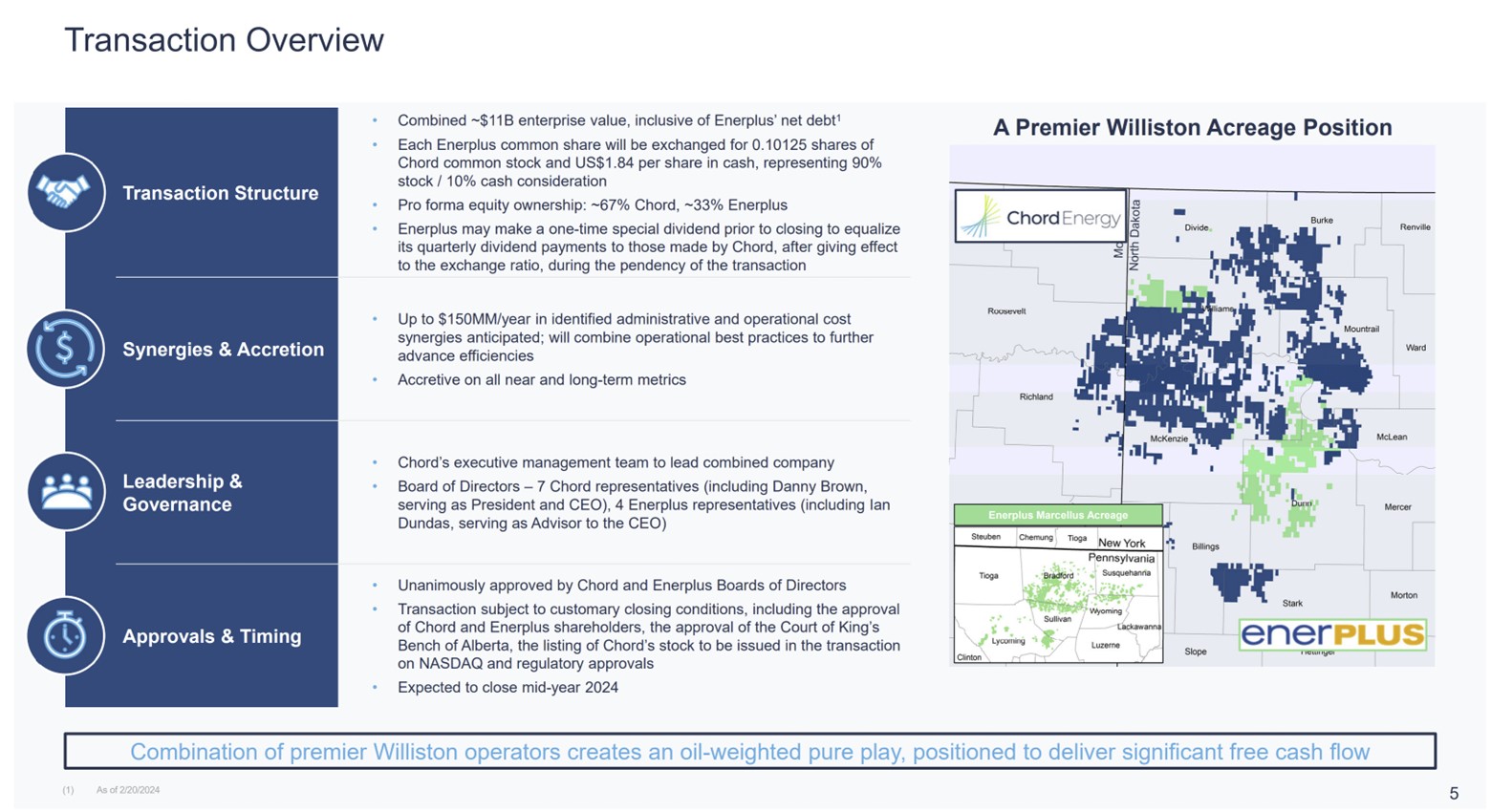

Chord Energy is acquiring Enerplus in a cash-and-stock deal, valuing the target at about $3.9 billion (including the assumption of debt). It's paying 90% of the $3.4 billion equity value in stock (0.10125 of its shares for each share of Enerplus) and the other 10% in cash ($1.84 per share). The transaction will create an $11 billion oil and gas company by enterprise value.

Enerplus is a near-perfect strategic fit for Chord Energy:

Image source: Chord Energy.

As the map on that slide shows, the acquisition will increase Chord Energy's acreage position in the Williston Basin. The combined company will have nearly 1.3 million net acres and produce 279,000 barrels of oil equivalent per day (BOE/d). That will make it the top producer in the region. The increased scale drives Chord's view that it can capture up to $150 million in annual cost savings. While Enerplus also owns a non-operated position in the gas-rich Marcellus shale, Chord could seek to sell those assets to further enhance its financial position.

The cost savings from the combination will help increase Chord's free cash flow. The combined company expects to produce around $1.2 billion in free cash this year (up from $800 million as a stand-alone company). Chord intends to return 75% of that money to shareholders via a base dividend, variable dividends, and share repurchases.

Chord reaffirmed its current base dividend rate ($5 per share annually). Meanwhile, it recently declared its latest variable dividend at $2 per share for the fourth quarter. Annualizing the most recent combined payment puts its dividend yield at 8%. Given its enhanced free cash flow, Chord could continue paying significant dividends following its Enerplus merger.

Another option off the table for Devon

Reuters reported earlier this month that Devon approached Enerplus with an acquisition offer. Buying Enerplus would have enabled Devon to significantly enhance its scale in the Williston Basin, where it's a much smaller producer (54,000 BOE/d compared to Enerplus' 78,000 BOE/d).

Devon was also reportedly among the many companies evaluating a potential offer to acquire CrownRock before Occidental Petroleum's $12 billion deal. CrownRock would have significantly bolstered its already world-class position in the Delaware Basin. Reuters also reported that Devon had discussed a merger with Marathon Oil. However, those talks ended because they could not agree on terms.

Devon is one of many oil companies seeking to participate in the current consolidation wave washing over the oil patch. Exxon kicked things off by agreeing to acquire Pioneer NaturalResources for over $60 billion last year. Chevron followed with a deal to buy Hess for around $60 billion, while Diamondback Energy agreed to a $26 billion takeover of privately held Endeavor Energy Resources.

Even with so many targets taken, Devon has plenty of options. It could circle back to Marathon. The multi-basin producer would be an excellent strategic fit. It could also consider Permian Resources, which, like Devon, has a strong position in the Delaware Basin, or Matador Resources, which operates in the Delaware, Eagle Ford (where Devon also operates), and the gassier Haynesville shale and Cotton Valley plays. The key will be to find a target that's a strong strategic fit to enhance its scale and free cash flow. Securing the right deal at the right price could enable Devon to boost its free cash flow, giving it more money to pay dividends.

Waiting for the right opportunity

Devon Energy's transformational merger with WPX Energy in 2021 created a lot of value for shareholders. It enhanced its free cash flow, giving it the fuel to launch its very popular fixed-plus-variable dividend framework. Others, like Chord Energy, have copied that playbook. It's now acquiring the same company Devon wanted to buy, which should fuel more dividends for its investors.

However, losing out on another acquisition isn't the end of the world for Devon. There are still plenty of opportunities to participate in the current consolidation wave. It could deliver another transformational phase of value creation if it can wait for the right deal to emerge.

Should you invest $1,000 in Devon Energy right now?

Before you buy stock in Devon Energy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Devon Energy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

Matt DiLallo has positions in Chevron. The Motley Fool has positions in and recommends Chevron and Enerplus. The Motley Fool recommends Occidental Petroleum and Pioneer Natural Resources. The Motley Fool has a disclosure policy.