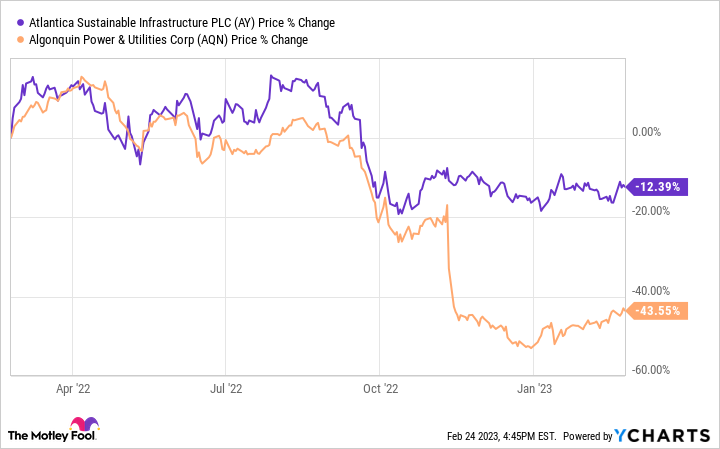

The past year has been brutal for investors in Algonquin Power & Utilities(NYSE: AQN). The utility has lost half its value because of deteriorating financial performance and concerns about its balance sheet because of its pending acquisition of AEP's Kentucky Power assets. Those issues have also weighed on shares of Atlantica Sustainable Infrastructure(NASDAQ: AY). That's because Algonquin is the largest shareholder of the renewable energy and sustainable infrastructure owner.

However, a big potential catalyst for both stocks has emerged. Atlantica recently revealed that it had commenced a review of its strategic alternatives. That process could maximize value for shareholders, including Algonquin.

Considering its options

Atlantica Sustainable Infrastructure recently announced that it had started exploring and evaluating potential strategic alternatives that might be available to enhance shareholder value. Algonquin, which is the company's largest shareholder, supports the plan.

While Atlantica believes it has attractive growth and other opportunities ahead, it will review other potential options, given the situation with Algonquin and its impact on the share price. Possible alternative options include selling the company, divesting select assets, or bringing in a new keystone investor.

There's no guarantee this process will lead to any changes. However, launching a strategic review alerts potential suitors that the company is open to considering its options, which increases the potential for a deal. Meanwhile, Algonquin's situation makes a transaction even more likely.

Algonquin seems motivated to sell

Algonquin is facing lots of challenges these days. That's forcing the utility to evolve so it can adapt to these changes. The company believes its controversial acquisition of Kentucky Power from AEP will help drive its long-term energy transition strategy.

However, investors and analysts don't like the deal because it would increase debt and potentially weaken the company's balance sheet. That's leading it to take several actions to avoid that situation, including slashing its dividend and refocusing its portfolio by targeting about $1 billion of asset sales.

Analysts believe the company could also sell its 43% stake in Atlantica. While that company's stock price has been under pressure this year, it has a market cap of over $3 billion. That puts Algonquin's interest in the company currently worth around $1.3 billion.

There should be no shortage of interested bidders

Analysts see a potential Algonquin sale of its stake in Atlantica as an upside catalyst for that company. Based on this thesis, RBC Capital analyst Shelby Tucker upgraded Atlantica's stock last month to outperform with a $34 price target. Tucker believes Algonquin could sell its entire stake to another company that would become a long-term investor and sponsor for Atlantica. That could bolster the company's long-term growth prospects if the acquiring entity has a pipeline of assets or development projects that Atlantica could acquire to grow its cash flow and dividend.

Another potential option is Atlantica could agree to sell itself to a private equity fund at a premium. There were some rumors last fall that the company had received takeover interest. Private equity funds are currently brimming with cash. For example, the big-three private equity giants Blackstone, KKR, and Brookfield Asset Management(NYSE: BAM) entered 2023 with almost $400 billion of dry powder between them. The sector is investing billions of dollars into sustainable infrastructure because of its attractive returns and growth prospects, which have only gotten better since the passage of the Inflation Reduction Act last year. Atlantica could therefore be an appealing target for a private equity fund seeking to invest more capital into the sector, especially given its lower share price resulting from the Algonquin situation.

Brookfield stands out as a potentially interested bidder. Its renewable energy subsidiary, Brookfield Renewable (NYSE: BEPC)(NYSE: BEP), has the balance sheet and global scale to complete a transaction with Atlantica. It could acquire Algonquin's stake and become the keystone investor in Atlantica or take the entire company private. Acquisitions are a key aspect of Brookfield Renewable's long-term growth strategy.

A potential win-win outcome

Atlantica Sustainable Infrastructure has decided to explore its strategic options. While that process might not result in a transaction, the probability seems high, given Algonquin's situation. It could provide Algonquin with a much-needed cash infusion while enhancing value for Atlantica's other investors. Both stocks have a potential near-term catalyst that could boost their share prices.

10 stocks we like better than Algonquin Power & Utilities

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Algonquin Power & Utilities wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of February 8, 2023

Matthew DiLallo has positions in Atlantica Sustainable Infrastructure Plc, Blackstone, Brookfield Asset Management, Brookfield Renewable, Brookfield Renewable Partners, and KKR and has the following options: short June 2023 $60 puts on Blackstone and short March 2023 $45 puts on KKR. The Motley Fool has positions in and recommends Blackstone, Brookfield Asset Management, Brookfield Renewable, and KKR. The Motley Fool recommends Brookfield Renewable Partners. The Motley Fool has a disclosure policy.