Coal stocks like Peabody Energy(NYSE: BTU) and Consol Energy(NYSE: CEIX) may be among 2022's biggest winners, but don't look for the same sort of bullish results in 2023. Investors planning to stick with these stocks for the long haul may want to brace themselves. The circumstances driving thermal coal names higher this year are already unwinding as we prepare to flip the calendar.

A perfect storm

Natural gas prices were certainly high in late 2021, but few people expected the commodity's price to continue racing to highs reached in the middle of this year. With no other cost-effective choices readily available, many of the world's electricity production plants were forced to revert to generating power by burning coal rather than gas, even if only temporarily. To this end, the International Energy Agency estimates worldwide coal consumption will rise 1.2% this year, eclipsing 8 billion tonnes of usage for the first time.

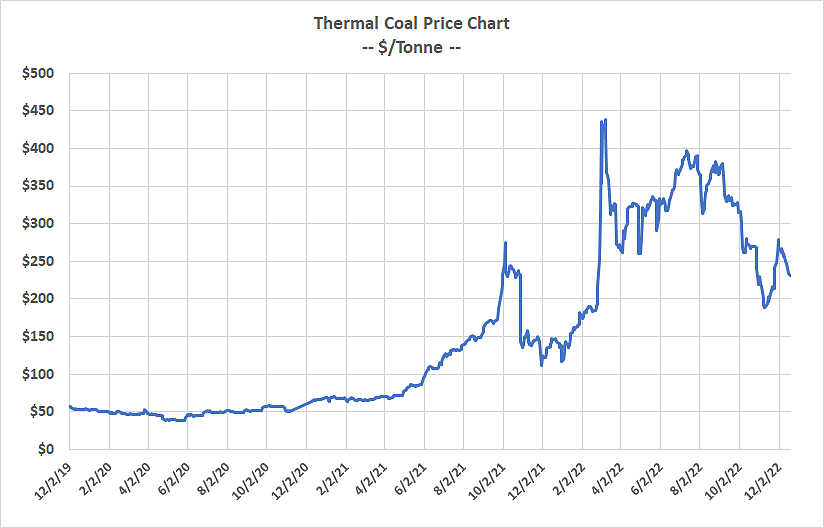

It's proven a boon for miners like the aforementioned Consol Energy and Peabody Energy, which dig up the thermal coal well suited for this application. Stocks of these two outfits are up 182% and 220% year to date, respectively, fueled by what's been roughly a tripling of thermal coal prices since the advance began back in 2020. Shares of thermal coal miners Arch Resources and Alliance Resource Partners have been star performers this year as well, even if not as strong as Peabody and Consol.

Don't look for coal consumption to slow in 2023 either. The International Energy Agency (IEA) is forecasting the coming year's consumption of coal will look much like this year's. China -- already the world's biggest user of the fossil fuel, accounting for roughly half the global market -- is projected to burn more coal in 2023 than it will in 2022.

What is likely changing for the worse, however, is the high price of coal many miners have been enjoying lately.

The thermal coal party is winding down

The coal mining industry can expand or shrink its capacity as needed. What coal miners can't do, though, is expand or shrink their capacity on the fly. It takes time to bring more production online; it even takes time to take capacity offline.

The industry didn't have much time to adapt coming out of 2021 and through 2022 when, among other things, Russia invaded Ukraine, fanning the flames of higher coal prices. It now seems they've had enough time to address these unique challenges.

Just this September, Alliance Resource Partners announced plans to develop a new mine in Henderson, Kentucky, defying efforts to phase out usage of the fossil fuel. Meanwhile, India, China, and Indonesia all intend to ramp up their production of thermal coal in 2023. Although most of that increased output also will be used by and within these three nations, the decision still frees up global supplies of the energy-creating mineral.

That's why Fitch Ratings is forecasting a sizable dip in the price of thermal coal, from around $300 per tonne now to $220 per tonne next year and en route to less than $100 per tonne in 2024. Indeed, the price contraction may already be underway.

Data source: Business Insider. Chart by author.

And it's not just Fitch fearing the impact of demand headwinds coupled with improving supplies. Consol Energy's senior vice president, Dan Connell, recently commented, "We're still projecting US domestic coal production to actually decrease in 2023 versus 2022," pointing to broader, renewed efforts to replace thermal coal with cleaner power-producing options. Connell's view is arguably a proxy for the entire industry's current worries.

To this end, Fitch Ratings estimates the world's coal mining companies will suffer nearly a 7% decline in revenue in the coming year, followed by nearly an 8% sales dip in 2024. Earnings before interest, taxes, depreciation, and amortization (EBITDA) margins, in turn, are projected to fall from this year's 42% to 37.8% in 2023 and 32.9% by 2024.

More risk, less reward ahead

It's not all bad news. The aforementioned Alliance Resources has inked deals assuring the sale of 5.6 million tons of thermal coal at "prices supporting higher margins" through 2025. Peabody used this year's windfall to pay down debt. Its total liabilities stood at just under $2.8 billion as of the end of September, down from over $3.1 billion a year earlier. It could be enough to allow the miner to start paying dividends -- at least according to B Riley Securities analyst Lucas Pipes. Certainly a few miners have derived some sustainable benefit from the business's unusual circumstances.

Think bigger-picture though. Not all mining thermal coal mining companies were able to lock in price contracts, and certainly any new customers will be paying then-current coal prices Fitch expects to fall in 2023 and then fall again in 2024

Interest rates have also soared this year, setting the stage for costlier capital in the foreseeable future. And most coal miners were already paying above-average interest rates because they pose above-average risk to lenders. The single-biggest loan on Consol's books is costing the company 11% per year, and that credit line's interest rate is a floating rate that could continue to rise. Other miners are facing similar interest rate challenges.

Connect the dots. This new paradigm isn't proving problematic for coal companies just yet, or their stocks. Given how the thermal coal market is primed to shift back to pre-2021 pressures and prices though, these stocks could be up-ended with little to no warning. Tread lightly if you're planning on sticking with any of these holdings.

10 stocks we like better than Consol Energy

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Consol Energy wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2022

James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.